As foreign central banks dump U.S. bonds to defend their own economies, rising yields and shrinking demand threaten to destabilize the financial system underpinning American power.

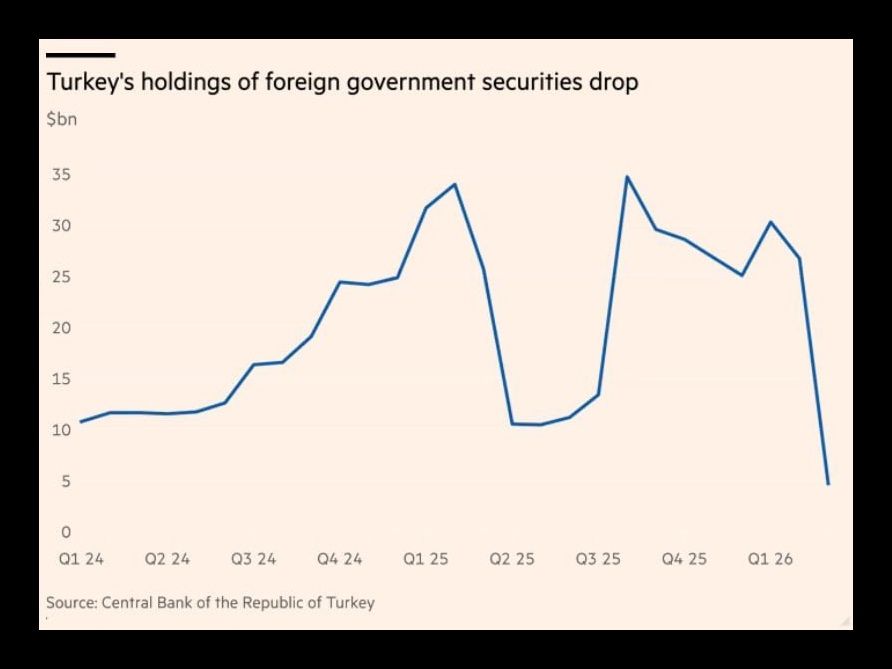

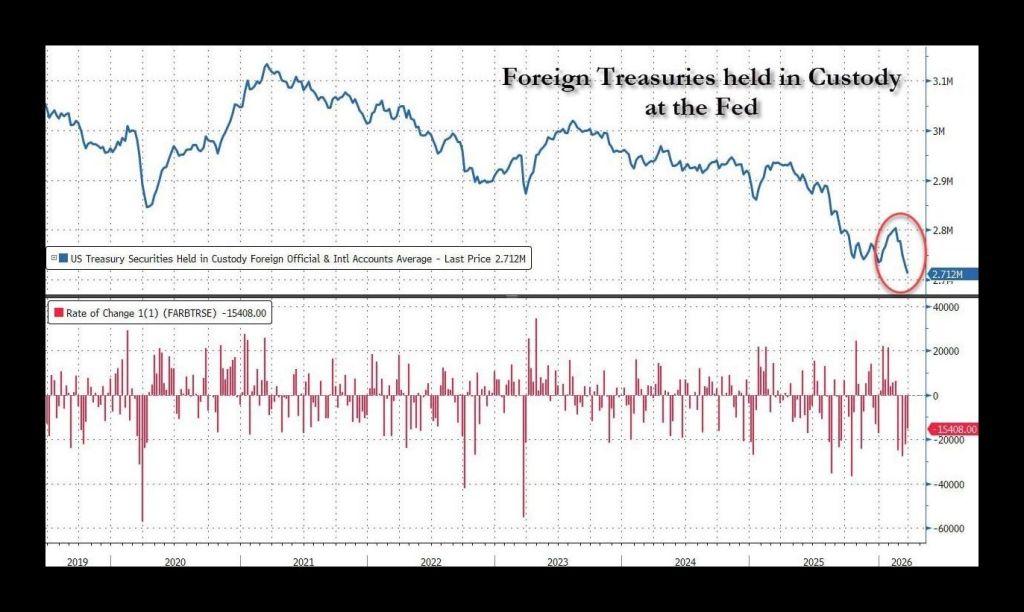

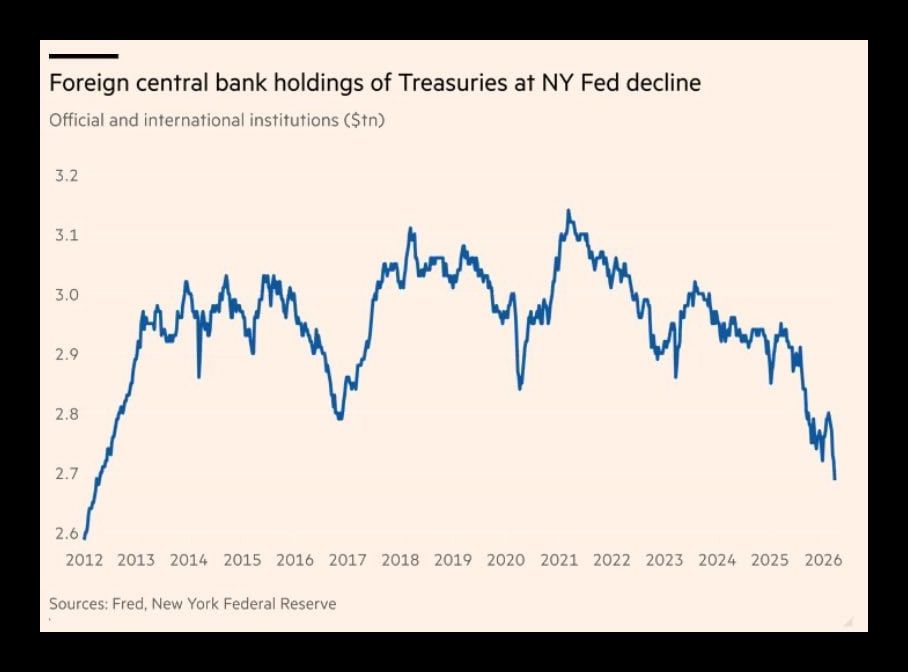

A financial shock is moving through the global system as foreign central banks offload tens of billions of dollars in U.S. Treasuries in a matter of weeks in favor of gold as a safe haven asset. The scale, roughly $82 billion in a single month, signals more than routine portfolio adjustment. It reflects mounting stress across currency markets as countries scramble to defend their own economies amid rising energy prices and geopolitical escalation. As oil surges in response to conflict involving Iran, import-dependent economies are being squeezed, forcing central banks in countries such as Turkey and India to sell dollar-denominated assets to stabilize their currencies and contain inflationary pressure. Turkey accounted for roughly $22 billion of the sell-off, while India likely contributed in the range of $15-25 billion, based on historical intervention patterns and reserve dynamics, with the remainder spread across other emerging economies.

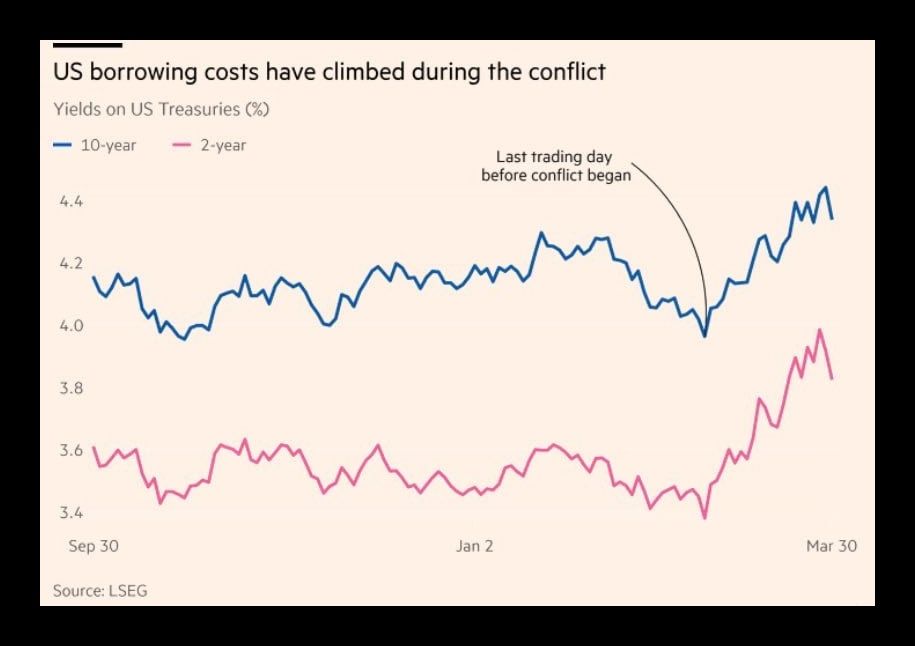

This wave of selling comes at a uniquely vulnerable moment for the United States. Washington faces the need to refinance an enormous volume of existing obligations, on the order of $10 trillion within a single year, while also funding ongoing deficits. Under normal conditions, global demand for Treasuries acts as a stabilizing force, keeping borrowing costs manageable. But when key external buyers begin stepping back or liquidating holdings, that equilibrium starts to fracture. The consequence is straightforward but severe: yields rise, borrowing costs increase, and the fiscal burden compounds rapidly.

The deeper issue is structural. For decades, the U.S. has relied on a global system in which surplus nations recycle capital into its debt markets, effectively subsidising American borrowing. This arrangement depends on confidence, confidence in the dollar, in U.S. financial stability, and in geopolitical alignment. When countries are forced to choose between defending their own currencies and holding U.S. debt, that confidence begins to erode at the margins. Each sale of Treasuries to prop up a domestic currency is rational in isolation, but collectively it creates upward pressure on U.S. yields and signals a gradual weakening of external support.

This is where the concept of the “Treasury Trap” becomes critical. If foreign demand softens at the same time issuance surges, the U.S. faces a narrowing set of options. Domestic buyers, banks, pension funds, and households, can absorb some supply, but not indefinitely at current scales. The Federal Reserve could step in more aggressively, effectively monetizing debt, but that risks reigniting inflation and undermining confidence in the dollar. Alternatively, higher interest rates can attract buyers, but at the cost of slowing the domestic economy and sharply increasing the government’s debt servicing burden.

The consequences cascade. Rising yields don’t just affect government borrowing; they ripple across mortgages, corporate debt, and consumer credit. A sustained increase in rates tightens financial conditions, reduces investment, and pressures already leveraged sectors. At the same time, higher debt servicing costs crowd out other government spending, forcing difficult fiscal trade-offs or further borrowing, deepening the cycle.

What makes the current moment particularly volatile is the interaction between geopolitics and finance. Energy shocks tied to conflict are forcing countries to prioritise immediate stability over long-term investment strategies. In doing so, they are unintentionally stress-testing the very system that has underpinned U.S. financial dominance. If this pattern accelerates, if more countries begin reducing exposure not just temporarily but structurally, the result is not a sudden collapse, but a steady repricing of U.S. debt and a more fragile equilibrium.

The central question besides whether the U.S. can issue debt, it can, but at what cost, and with whose support. If external buyers retreat while internal constraints tighten, the burden shifts inward, and the price of maintaining the system rises sharply. That is the core risk embedded in the current selloff: not an immediate crisis, but the early stages of a feedback loop in which higher costs, weaker demand, and geopolitical fragmentation reinforce one another.

Authored By: Global GeoPolitics

Thank you for visiting. This is a reader-supported publication. If you believe journalism should serve the public, not the powerful, and you’re in a position to help, becoming a PAID SUBSCRIBER truly makes a difference. Alternatively you can support by way of a cup of coffee:

https://buymeacoffee.com/ggtv |

https://ko-fi.com/globalgeopolitics |

Bitcoin: 3NiK8BoRZnkwJSHZSekuXKFizGPopkE7ns

Leave a comment