You can suppress futures prices, but you cannot suppress physical scarcity and markets will eventually reflect that reality.

The collapse in gold and silver prices observed yesterday reflected a deliberate intervention rather than a market driven repricing event, given the scale, timing, sequencing, and institutional mechanisms involved. Gold declined by more than twelve per cent intraday, while silver experienced losses approaching thirty five per cent, destroying several trillion dollars of nominal market value within hours. Such movements lie well outside historical volatility ranges for these assets under conditions where no macroeconomic data releases, military escalations, banking failures, or monetary policy announcements were present, a point consistent with volatility analyses published regularly by the Bank for International Settlements.

Price expectations in financial markets function as coordination devices, anchoring behaviour across participants through shared assumptions regarding future states of the system. George Soros has long argued that market prices do not merely reflect fundamentals but actively influence them, a dynamic he described as reflexivity. In precious metals markets, expectations play a particularly central role because physical supply adjusts slowly, while paper leverage responds immediately. When expectations become strongly unidirectional during extended rallies, the system becomes increasingly vulnerable to abrupt reversals triggered through institutional control points rather than decentralised selling pressure. January had produced the strongest silver performance in decades, with gains exceeding sixty five per cent and widespread projections extending toward substantially higher prices.

The expectations environment entering the final trading day of January was therefore characterised by optimism, elevated leverage, and confidence in continued upside momentum. Data published by the Commodity Futures Trading Commission showed historically high speculative long exposure, while options markets reflected a pronounced skew toward further price appreciation. Similar configurations preceded earlier episodes in which sharp reversals followed institutional action rather than changing fundamentals, including the silver collapses of 1980 and 2011, both of which were later examined in congressional and academic reviews.

The intervention mechanism activated precisely at the New York open, the moment of maximum global liquidity and algorithmic alignment. Within minutes, sell orders measured in millions of ounces were executed into the futures market, overwhelming available bids and forcing prices through known liquidity gaps. Research on market microstructure by Jean-Philippe Bouchaud and J. Doyne Farmer has demonstrated that large orders executed rapidly can generate price dislocations unrelated to new information, a finding directly relevant to the observed price action.

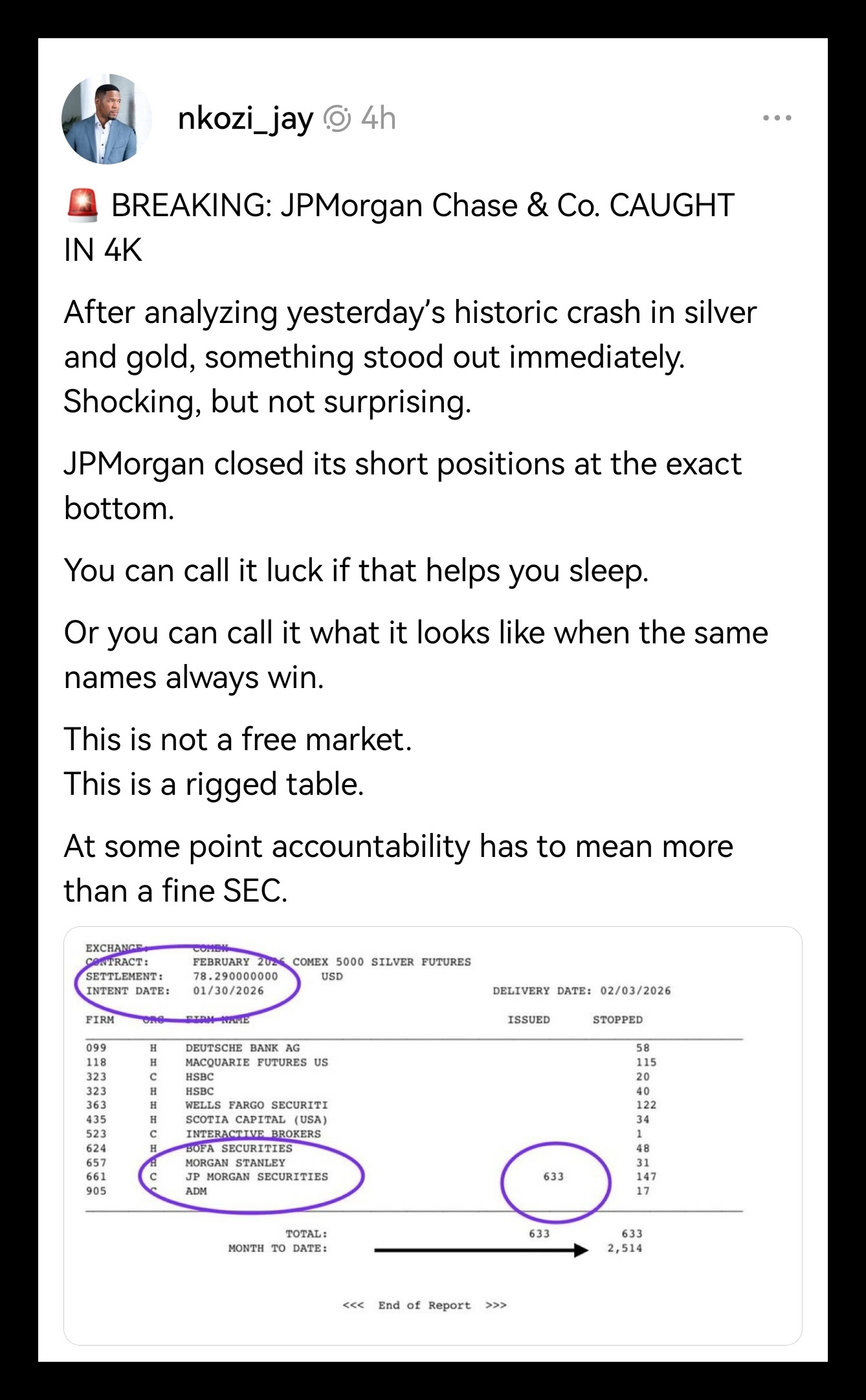

The scale and coordination of selling eliminated the likelihood of decentralised profit taking or spontaneous sentiment reversal. A rational trader seeking efficient exit would not liquidate positions in a manner that guarantees maximal adverse price impact. The observed behaviour therefore aligns with intent to move prices rather than optimise execution, a distinction recognised in regulatory literature and enforcement actions concerning market manipulation.

The margin framework administered by the CME Group played a central role in transforming initial price pressure into systemic collapse. As prices declined, margin requirements were raised rapidly, forcing leveraged participants to post additional collateral immediately or liquidate positions. Comparable mechanisms were documented during earlier precious metals dislocations, most notably during the May 2011 silver collapse, when the CME implemented a sequence of margin increases within a compressed period. Analysts at the time noted that margin policy in these markets operates with significant discretion and asymmetry, tightening rapidly during rising price environments while easing more slowly during declines.

Margin calls operate directly on expectations by converting unrealised losses into immediate liquidity demands. Once margin thresholds are breached, participants are compelled to sell regardless of longer term outlook or physical fundamentals. The resulting liquidation cascade is mechanical rather than psychological, producing outcomes driven by balance sheet constraints rather than changing beliefs. Research by Tobias Adrian and Hyun Song Shin at the Federal Reserve Bank of New York has shown that leverage responds endogenously to asset prices, amplifying both upward and downward movements.

The intervention therefore functioned less as a corrective process and more as a coordinated reset of market conditions, using futures selling to initiate the move and margin escalation to ensure broad participation. Comparable approaches were employed during earlier episodes in which exchanges and regulators acted to stabilise systems experiencing destabilising expectation dynamics. In such cases, the objective was not immediate price discovery but the disruption of self reinforcing belief structures that encouraged further leverage expansion.

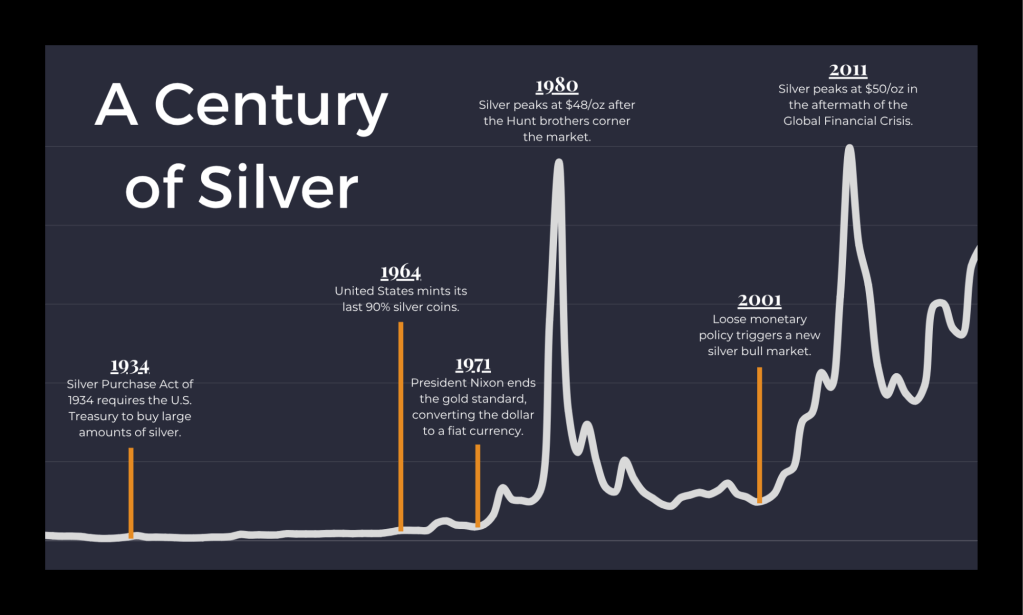

The 1980 silver collapse provides an early reference point. Rapid price appreciation driven by inflation fears and concentrated accumulation culminated in exchange imposed rule changes, sharply higher margins, and liquidation only settlement requirements. Prices collapsed abruptly, transferring losses to leveraged long participants while preserving exchange solvency and institutional continuity. A subsequent investigation by the United States Senate concluded that exchange rule changes materially altered market outcomes independent of new economic information.

The 2011 episode followed a similar pattern under modern derivatives infrastructure. Silver prices rose sharply amid quantitative easing and sovereign debt concerns, drawing substantial retail and institutional participation. As prices accelerated, the CME introduced multiple margin increases over a short period, sharply raising capital requirements. Prices declined by more than fifty per cent within weeks, despite stable physical demand and constrained mine supply, a sequence widely analysed by academics and industry specialists as evidence that institutional mechanics rather than fundamentals drove the reversal.

The present episode mirrors these precedents but unfolds within a materially altered geopolitical and monetary context. East Asian markets now exert greater influence on physical demand, with China functioning as the largest marginal buyer of both gold and silver. The Shanghai Gold Exchange settles contracts in physical metal, anchoring domestic price formation more closely to deliverable supply than to cash settled derivatives, a structure described in detail by Chinese monetary economists such as Yu Yongding and in official publications of the People’s Bank of China. Elevated Western prices tend to accelerate physical flows toward Asia, increasing pressure on custodial inventories in London and New York.

Chinese authorities have pursued a long term strategy of increasing precious metals holdings while gradually reducing exposure to dollar denominated assets. This approach has been characterised in academic research and official statements as a risk management strategy rather than a speculative posture. Higher precious metals prices strengthen reserve positions and signal monetary stress within Western systems. Sudden price collapses therefore reduce accumulation efficiency and slow physical outflows from Western vaulting systems.

Silver presents additional sensitivity due to persistent physical deficits driven by industrial demand, particularly in sectors concentrated in East Asia such as photovoltaics, electronics, and advanced manufacturing. Annual mine supply has repeatedly fallen short of total demand, with deficits bridged through inventory drawdowns, leasing arrangements, and paper claims, according to data compiled by the Silver Institute and corroborated by independent supply-demand studies. Rising prices increase the likelihood of delivery requests that expose the limits of available physical stocks.

Western vault inventories have been drawn down over several decades through sales, leasing, and structural disinvestment, leaving limited buffers against sustained delivery demand, a process documented in reports by the United Kingdom National Audit Office and bullion market research bodies. When industrial actors or sovereign entities seek delivery in size, the system relies on cash settlement, contract rolling, or price suppression to manage strain. Futures markets therefore operate as pressure valves, releasing physical stress through price adjustment rather than delivery failure.

From a game theory perspective, the intervention reflects a dominant strategy within a repeated interaction framework. Allowing prices to continue rising increases the probability of delivery pressure, reputational damage, and accelerated diversification away from Western financial assets. Forcing a sharp repricing imposes losses on leveraged participants while preserving institutional continuity. Thomas Schelling’s work on strategic behaviour emphasised that effective action often depends on changing the structure of incentives rather than persuading participants, a principle applicable to the present case.

Chaos theory further clarifies the necessity of magnitude. Research on nonlinear financial systems shows that incremental interventions often fail once markets approach critical thresholds. Larger shocks can move the system toward a new equilibrium characterised by reduced leverage and diminished speculative participation. The scale of the recent collapse therefore reflects underlying system fragility rather than disproportionate response.

The absence of contemporaneous policy announcements, economic data releases, or geopolitical events reinforces the interpretation that causality resided within market structure rather than external information. Limited immediate commentary from major institutions during the event is consistent with prior episodes in which exchange level actions later emerged as primary drivers.

Looking forward, the immediate effect is likely to be reduced speculative participation, lower leverage, and temporary stabilisation of custodial systems. Physical demand in East Asia is likely to increase at lower prices, accelerating inventory transfer rather than resolving structural scarcity. Repatriation requests for gold are unlikely to diminish, as lower prices reduce fiscal and political costs for requesting states, a trend already visible in central bank disclosures.

Under conditions of increasing multipolarity, repeated interventions may prove less effective than in prior decades. Alternative settlement systems, sustained diversification away from United States Treasuries, and declining confidence in Western custodial arrangements reduce the long term efficacy of expectation management through derivatives markets. While such interventions remain tactically effective, their strategic capacity to restore durable confidence continues to weaken.

To sum it up, yesterday’s market disruption followed directly from the intervention imposed by the CME Group in December. The margin increases succeeded in reducing leverage, but they did not address underlying physical supply constraints. Subsequent price declines therefore reflect forced liquidation rather than improved market balance.

At the same time, physical silver prices in Asia have diverged sharply from Western futures benchmarks. In China, reported prices for deliverable silver have exceeded one hundred thirty dollars ($130) per ounce. In Japan, physical silver has reportedly traded close to one hundred forty dollars ($140) per ounce. These figures indicate independent price formation rather than temporary regional premiums.

This divergence weakens the role of Western futures markets as effective mechanisms of price discovery. When delivery becomes uncertain, futures prices increasingly reflect liquidity conditions instead of physical availability. Control over benchmark pricing therefore shifts toward jurisdictions that retain access to supply. The episode therefore represents a familiar short term stabilisation mechanism operating within an increasingly unstable long term structure. This has demonstrated that exchange-based interventions cannot substitute for physical market stability. As global finance becomes more multipolar, price management can delay reconciliation between paper claims and physical availability, but it cannot reverse the broader shift toward reserve diversification, repatriation, and reduced reliance on Western financial dominance.

Please check out my other recent related articles:

- https://globalgeopolitics.co.uk/2026/01/30/the-dollar-system-and-the-end-of-fiat-global-monetary-order/

- https://globalgeopolitics.co.uk/2026/01/17/collapse-of-western-power-and-the-global-system-in-2026/

- https://globalgeopolitics.co.uk/2026/01/06/oil-or-silver-the-real-stakes-behind-maduros-removal/

Authored By: Global GeoPolitics

Thank you for visiting. This is a reader-supported publication. I cannot do this without your support. You can support by way of a cup of coffee:

buymeacoffee.com/ggtv or

Leave a reply to albertoportugheisyahoocouk Cancel reply