How fifteen years of Chinese industrial policy produced an electric vehicle Detroit cannot match and why tariffs may be solving the wrong problem

General News Article | June 2026

(The headline image is the Geely Geome Xingyuan is a compact hatchback that sells for under $10,000)

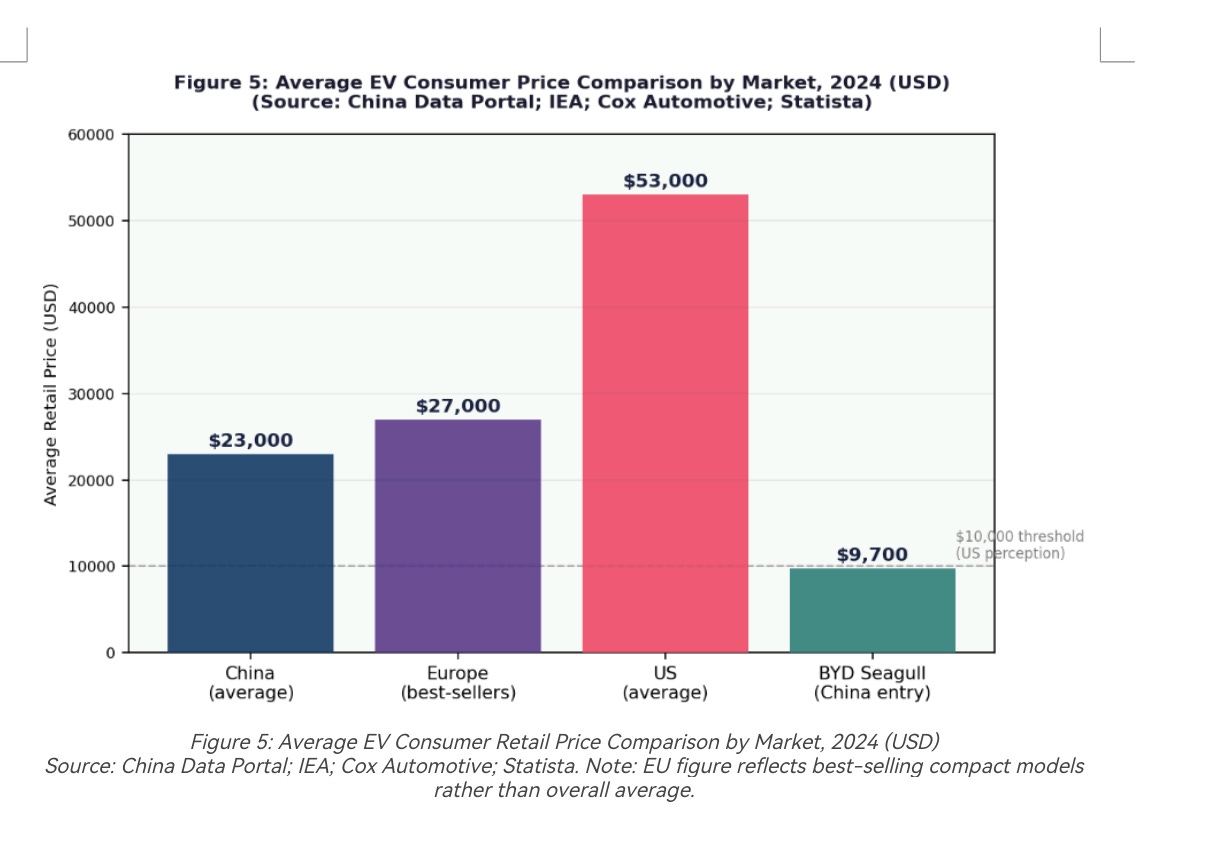

In 2023 BYD began selling a small electric hatchback called the Seagull in China for under $10,000. It has no pretensions, just a modest battery, a range built for city commuting, none of the touchscreen theatre that defines the American EV market. It is, in essence, an electric Nissan Micra. It is also the most concrete evidence yet that China has solved a problem the rest of the world has not, which was, how to make an electric car cheap.

The average electric vehicle sold in China in 2024 went for about $23,000. The average one sold in America went for more than $53,000. That gap, more than double, is not a temporary market quirk. It is the visible result of a deliberate, fifteen-year programme of state-directed industrial building, and it has left Washington and Brussels facing a question neither has fully answered: if you cannot make the cheap car, is the right response to wall it out, or to work out how to build one yourself?

A bet placed in 2010

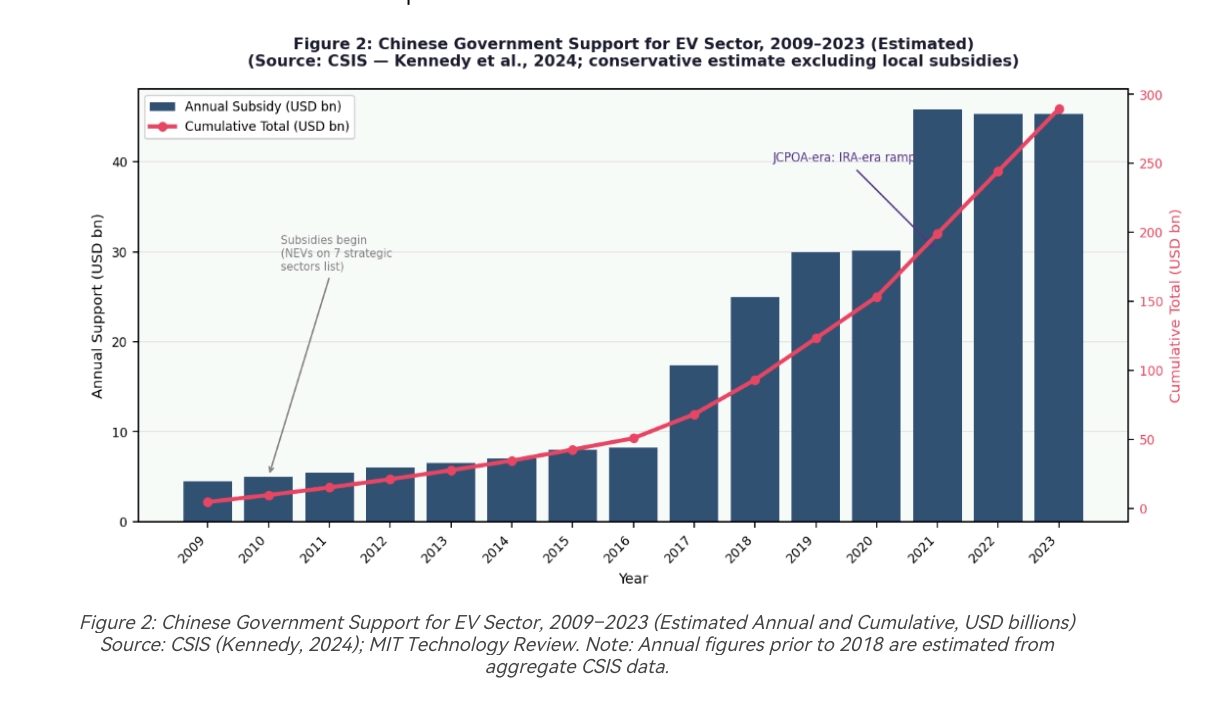

China’s pivot to electric vehicles did not begin as a climate policy. It began as a strategic workaround. When Beijing named “new energy vehicles” a priority sector under its twelfth five-year plan around 2010, the calculation was straightforward: in the internal combustion engine, a century of patents, supplier relationships and brand equity belonged to American, German and Japanese firms, and no amount of state spending would close that gap quickly. The electric motor offered a rare reset, a technology immature enough globally that manufacturing scale, rather than inherited expertise, would decide who won.

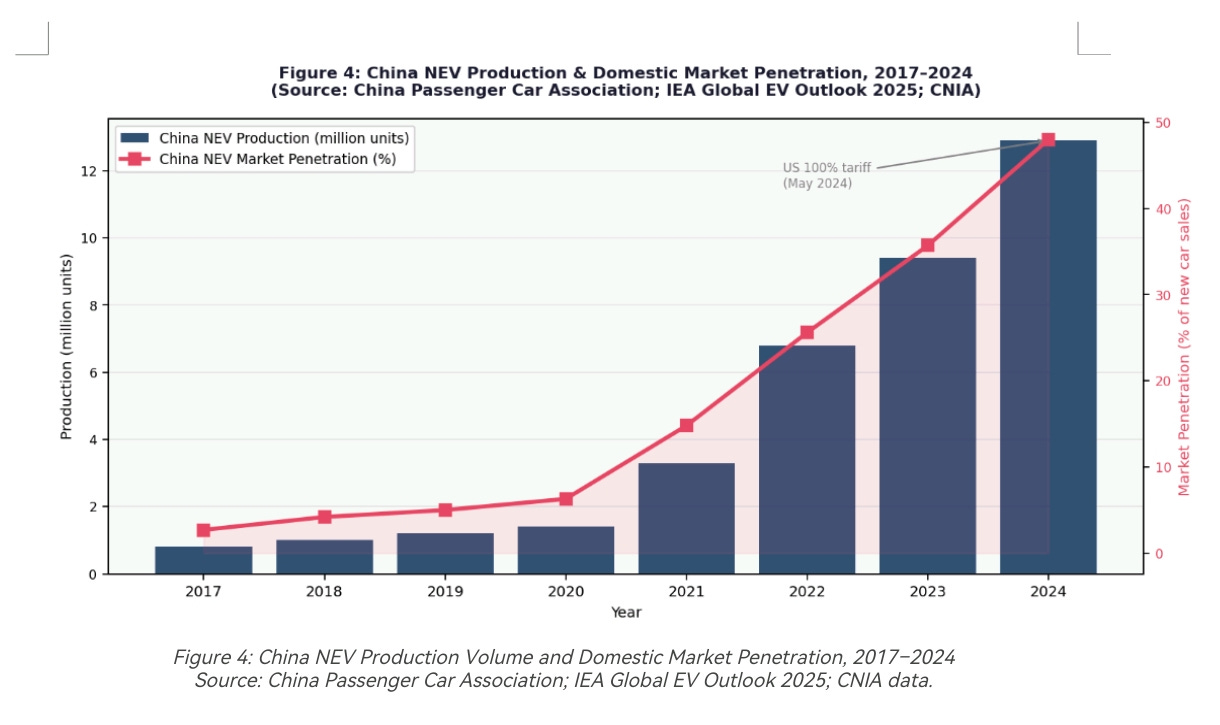

What followed was more than a few tax breaks. Between 2009 and 2023, Chinese national and local governments funnelled at least $230.9bn into the sector in the form of buyer rebates, infrastructure spending, research grants and tax exemptions, according to a 2024 analysis by Scott Kennedy at the Center for Strategic and International Studies, a figure he describes as conservative, since it excludes land subsidies, preferential utility rates and cheap loans from state banks. The CSIS data show something else notable, the subsidy per vehicle fell sharply, from roughly $13,860 in 2018 to under $4,600 in 2023, not because Beijing eased off (aggregate annual subsidies roughly tripled over the same period, to $45.3bn) but because sales grew even faster. By 2023, China’s subsidy per car was already lower than the $7,500 tax credit Washington offers American buyers today. The scaffolding, in other words, had started coming down just as the building could stand on its own.

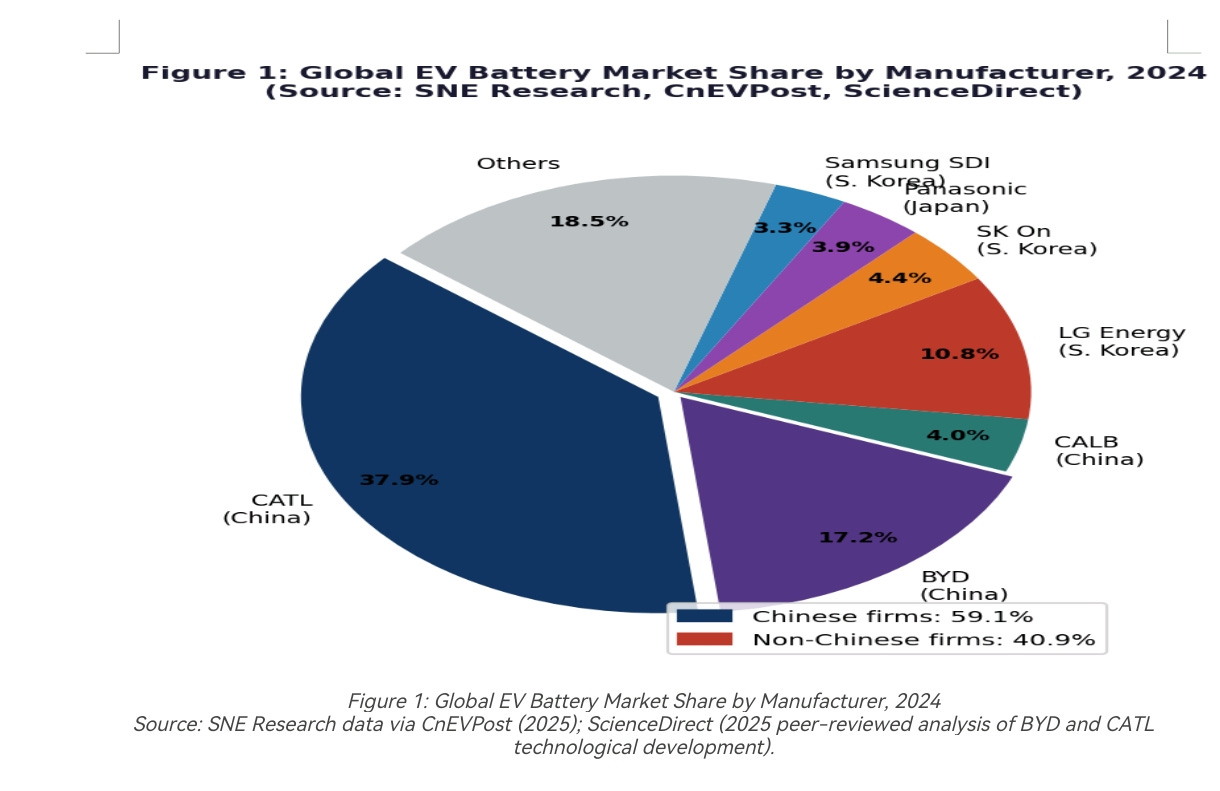

That building shows up most clearly in batteries, which account for 30–40% of an EV’s manufacturing cost, the single biggest lever on price. Contemporary Amperex Technology Co. Ltd, known as CATL, spun out of a Hong Kong-listed parent in 2011 and now supplies cells to Tesla, BMW, Volkswagen and Mercedes-Benz alongside Chinese carmakers. By 2024 it held a 37.9% share of global EV battery installations, according to the South Korean research firm SNE Research, the only supplier above 30%. BYD, which has made batteries since 2003, ranked second at 17.2%. Chinese firms together controlled around 59% of global battery capacity in 2024; by late 2025 that had risen to roughly 69%.

BYD’s own arc captures how state money and corporate strategy reinforced each other. It received $3.7bn in direct subsidies between 2018 and 2022, including $2.2bn in 2022 alone, meaningful, but not by itself decisive. What mattered more, according to a peer-reviewed study published in Research Policy in late 2025, was its “Blade Battery,” a lithium-iron-phosphate design engineered to survive nail-penetration tests without catching fire, which persuaded premium carmakers that a chemistry once confined to budget cars could go upmarket. Vertical integration, BYD makes its own cells, assembles its own vehicles and increasingly designs its own chips, let it shrug off the supply shocks that have battered rivals reliant on outside suppliers. In 2024 BYD sold 4.25m vehicles worldwide, more than double Tesla’s 1.8m, making it the world’s seventh-largest carmaker by volume.

What Tesla taught its rivals

There is a certain irony in Tesla’s role in all this. In 2018 China scrapped its decades-old rule requiring foreign carmakers to operate through joint ventures, and Tesla became the first wholly foreign-owned car manufacturer permitted on Chinese soil. Construction of Gigafactory Shanghai began in January 2019; cars were rolling off the line by December. Tesla’s own securities filings put the capital cost of the Shanghai plant at roughly 65% below its comparable American factory, a saving owed not to anything Tesla invented, but to an industrial ecosystem China had already built: clustered suppliers, logistics tuned for high-volume manufacturing, and permitting that moved faster than anything available in the West.

Tesla profited from that ecosystem. It also, inadvertently, taught it. Watching Tesla manufacture at scale on Chinese soil showed domestic rivals exactly what modern EV production economics could look like in their own factories. Where Tesla chased range, software and screen size, Chinese manufacturers, Wuling, BYD’s budget lines, later Xiaomi, went the other way: smaller batteries, shorter range tuned to how far people in cities actually drive, fewer expensive features, lower prices. The Seagull was the purest expression of that logic. By 2025, Tesla’s share of the Chinese market had slipped from about 9% to 6.5%, and deliveries from Shanghai fell 11.7% year-on-year in the second quarter as domestic rivals undercut it on price.

Washington’s answer is walls up, not factories

The American and European responses to this cost gap took different shapes, but shared a premise: compete on price, not by lowering it, but by excluding the competition.

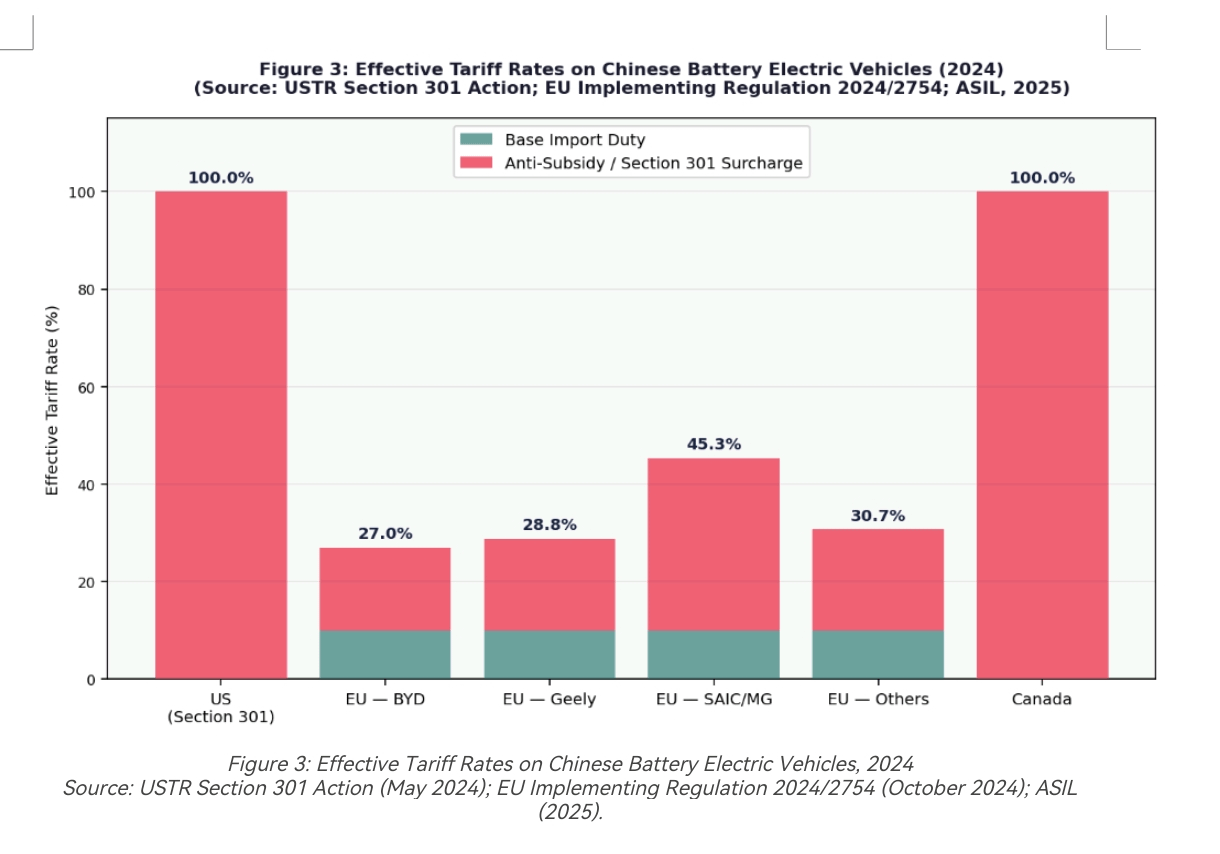

Washington’s tool was Section 301 of the 1974 Trade Act, which lets the US Trade Representative impose tariffs when a foreign country’s trade practices are deemed unreasonable. In May 2024 the Biden administration announced a 100% tariff on Chinese EVs, lifting the combined rate, layered atop existing duties, to 102.5%. A Chinese-made car leaving the factory gate at $10,000 becomes roughly $20,250 before shipping, certification and dealer margin are even added; by the time it reaches an American forecourt, the realistic landed price sits closer to $25,000–$30,000, and, crucially, it qualifies for none of the $7,500 federal tax credits that lower the price of rival vehicles. The mechanism does not need to be elegant to work. Stacked together, tariffs and tax-credit exclusions made the cheap Chinese car commercially unsellable in America without a single import actually being blocked at the border.

That second layer came from the Inflation Reduction Act of 2022, whose clean-vehicle credit requires North American assembly and bars battery components or critical minerals from so-called “foreign entities of concern”, a definition that, as written by the Treasury, captures most Chinese battery and mineral-processing firms by default. Congress has since pushed to tighten it further. The combined effect is a market in which the cheapest EVs available worldwide are, for American consumers, either priced out by tariffs or disqualified from the subsidies that make rival vehicles affordable. There was, in 2024, no legal route to an American buyer getting anything resembling Chinese pricing.

Brussels takes a different road, with similar results

The European Union reached a comparable destination by a more legally cautious path. The European Commission opened an anti-subsidy investigation in October 2023, unusually, without a formal complaint from EU industry and imposed definitive countervailing duties in October 2024, set firm by firm: 17% for BYD, 18.8% for Geely, 35.3% for SAIC, which had declined to cooperate with investigators. Tesla’s Shanghai-built exports drew a separate, lower rate of 9%, reflecting a smaller calculated subsidy benefit. Stacked on the EU’s standard 10% car tariff, total rates range from 17.8% to 45.3%.

Germany and Hungary voted against the measure, a reflection of how exposed BMW, Volkswagen and Mercedes-Benz are to Chinese retaliation in a market that supplies a third or more of their global revenue. The vote exposed a fault line that tariffs have not resolved which a Rhodium Group study in 2023 estimated EU duties would need to reach 45–55% to genuinely deter Chinese exporters at current margins. SAIC’s rate clears that bar. BYD’s does not and CSIS analysis suggests BYD still earns fatter margins selling into Europe, even after the duty, than it does at home. Chinese EV sales in Europe have kept growing regardless; BYD outsold Tesla there in April 2025. The company’s answer to the tariff wall has simply been to build inside it, with new plants in Hungary and Turkey producing cars that face no duty at all because they are no longer, technically, Chinese exports.

The cost of managing the market

Whether any of this is working depends entirely on what “working” was meant to mean.

If the goal was protecting American and European auto-sector jobs through a wrenching technological transition, the tariffs have arguably bought time. They created the conditions under which Ford’s BlueOval SK battery venture, General Motors’ Ultium partnership with LG, and Stellantis’s North American battery investments could be made without facing immediate Chinese price competition. That is a real, if narrow, achievement.

If the goal was accelerating the broader switch to electric vehicles, the underlying climate rationale most Western governments cite, the results look considerably worse. A National Bureau of Economic Research paper published in 2024 by David Autor and colleagues found that the first Trump administration’s earlier China tariffs produced little or no net employment gain and, in some cases, reduced household income, partly because tariffs on intermediate goods such as batteries and magnets raised costs for American manufacturers further up the chain. The University of Exeter’s Centre for International Trade Policy went further, calling the economic logic behind EV tariffs “complex and unclear” for the same reason.

The numbers on the ground bear that out. EVs made up 48% of new car sales in China in 2024; full battery-electric penetration in the EU passed 20%; Brazil’s EV sales jumped more than 90% in a year, driven largely by Chinese manufacturers selling vehicles in the $20,000–$25,000 range. American EV sales, by contrast, were essentially flat for stretches of 2024, with average transaction prices stuck above $50,000 and no real entry-level option for price-sensitive buyers. Tariffs did not make American-made EVs cheaper. They simply ensured nothing cheaper could compete with them, freezing the market at a price most Americans were not willing to pay, and trading a faster energy transition for a slower, more politically manageable one.

The harder problem underneath

The deeper issue for Western policymakers is that China’s advantage is not only a subsidy story, and tariffs cannot touch the part that isn’t. CATL’s newest “Qilin” battery design, which builds cooling channels directly into the cell to raise energy density to 255 watt-hours per kilogram, came out of more than a decade of accumulated manufacturing know-how, even if government subsidies to CATL itself rose from $76.7m in 2018 to $809.2m in 2023. Much of the critical-minerals processing that feeds battery production sits in China by virtue of years of capital investment in refining capacity that cannot be replicated on a few years’ notice, regardless of how much money Washington or Brussels throw at the problem. Roughly 70% of the nickel sulphate used in EV cathodes, for instance, is processed from Indonesian ore through Chinese-controlled facilities.

There is a complicating wrinkle, though. China’s own EV industry has a profitability problem: production capacity is estimated to run at roughly three times domestic demand, and as of August 2025 only three Chinese EV makers, BYD, Li Auto and Aito, were actually turning a profit, according to reporting in The Diplomat. Kennedy’s CSIS analysis makes a similar point: in a normally functioning market, that kind of overcapacity would force consolidation, not continued expansion. Whether Chinese overcapacity corrects itself or persists indefinitely will likely matter more to the industry’s trajectory over the next decade than any tariff schedule.

For now, the dispute sits unresolved in Geneva as much as in Washington or Brussels. China has filed World Trade Organisation complaints against the American, Canadian and European measures, while retaliating with its own investigations into European brandy, agricultural exports and large-engine combustion vehicles. The WTO’s appellate mechanism, however, has been effectively inoperable since 2017, after the US blocked new judicial appointments, meaning that whatever rulings emerge from these disputes face no real avenue of appeal. The trade architecture meant to referee this kind of conflict is, like so much else in the EV story, not quite built for the moment it is being asked to handle.

What is left is a genuine and, as yet, unresolved argument inside Western capitals: whether the energy transition is better pursued by competing, building the factories, the refining capacity, the supply chains that might one day produce a Western Seagull, or by managing the market until that becomes politically and industrially feasible. Germany’s carmakers, dependent on Chinese sales, want the former. Much of Washington’s current posture suggests the latter. Six years into the tariff era, the $23,000 car still does not exist outside China, and nothing in the current policy mix is designed to change that.

For the indepth advanced analysis paper please follow this link:

Authored By: Global GeoPolitics

If you prefer to make a one time donation in support of my work, you can do so by clicking any link below:

https://buymeacoffee.com/ggtv |

https://ko-fi.com/globalgeopolitics |

Bitcoin: 3NiK8BoRZnkwJSHZSekuXKFizGPopkE7ns

Leave a comment