An explanation of the policies that created a 518 trillion yen balance sheet and why exit is so difficult

For more than a decade, the Bank of Japan operated as the primary exception to every global monetary rule, a lonely laboratory where conventional economics was suspended in favour of a vast experiment in perpetual stimulus. Governor Kazuo Ueda, inheriting this machinery in April 2023, has spent the subsequent three years attempting to dismantle it without triggering a financial accident of historic proportions (4). The journey from the negative interest rate policy of minus 0.1 per cent, introduced in 2016, to a policy rate of 0.75 per cent by December 2025 represents the most significant monetary normalisation undertaken by a major central bank in the post-pandemic era (1;(8). Yet the true difficulty lies not in raising rates from deeply negative territory, but in convincing global markets that the BoJ can eventually withdraw its presence from the government bond market without sending borrowing costs soaring for the world’s most indebted nation.

The formal break with the past occurred in March 2024, when the BoJ terminated its eight-year experiment with negative interest rates alongside the Yield Curve Control framework that had artificially pinned ten-year Japanese government bond yields near zero per cent (9). This decision, the first rate hike in seventeen years, raised the overnight call rate to a range of zero to 0.1 per cent, finally acknowledging that the virtuous cycle of wages and prices which Haruhiko Kuroda had spent a decade trying to ignite might actually be materialising (4). Ueda pointed to the spring wage negotiations, known as Shunto, which delivered pay increases exceeding five per cent at many large firms, a level not seen since the early 1990s. For an economy that had spent three decades fighting falling prices and stagnant wages, this represented genuine structural progress rather than statistical noise. However, the BoJ’s accompanying commitment to continue purchasing roughly six trillion yen of government bonds each month revealed a deep institutional reluctance to let market forces determine (term borrowing costs (9).

What followed was a steady, almost hesitant, ascent in borrowing costs across 2025 and into 2026. Having moved to 0.25 per cent in July 2024 and then to 0.5 per cent in January 2025, the BoJ delivered another quarter-point increase in December 2025, bringing the policy rate to 0.75 per cent (1). Each move was telegraphed with extraordinary caution, reflecting Ueda’s academic background in monetary economics and his close study of the policy errors that defined the 1990s, when premature tightening by the BoJ arguably prolonged Japan’s deflationary malaise. By April 2026, however, the central bank opted to pause, holding the rate at 0.75 per cent despite sharply raising its inflation forecasts for the fiscal year to 2.8 per cent, nearly a full percentage point above its January projection (3; 10). This divergence between static rates and rising price expectations exposes the BoJ’s core dilemma: the inflation arriving on Japanese shores is not the domestically generated, demand-driven variety that Ueda sought, but an imported energy shock following military conflict in the Middle East (5). With Japan importing more than ninety per cent of its crude oil, the spike in prices acts as a tax on households and corporate margins, suppressing the very consumption that the BoJ needs to sustain a genuine wage-price spiral.

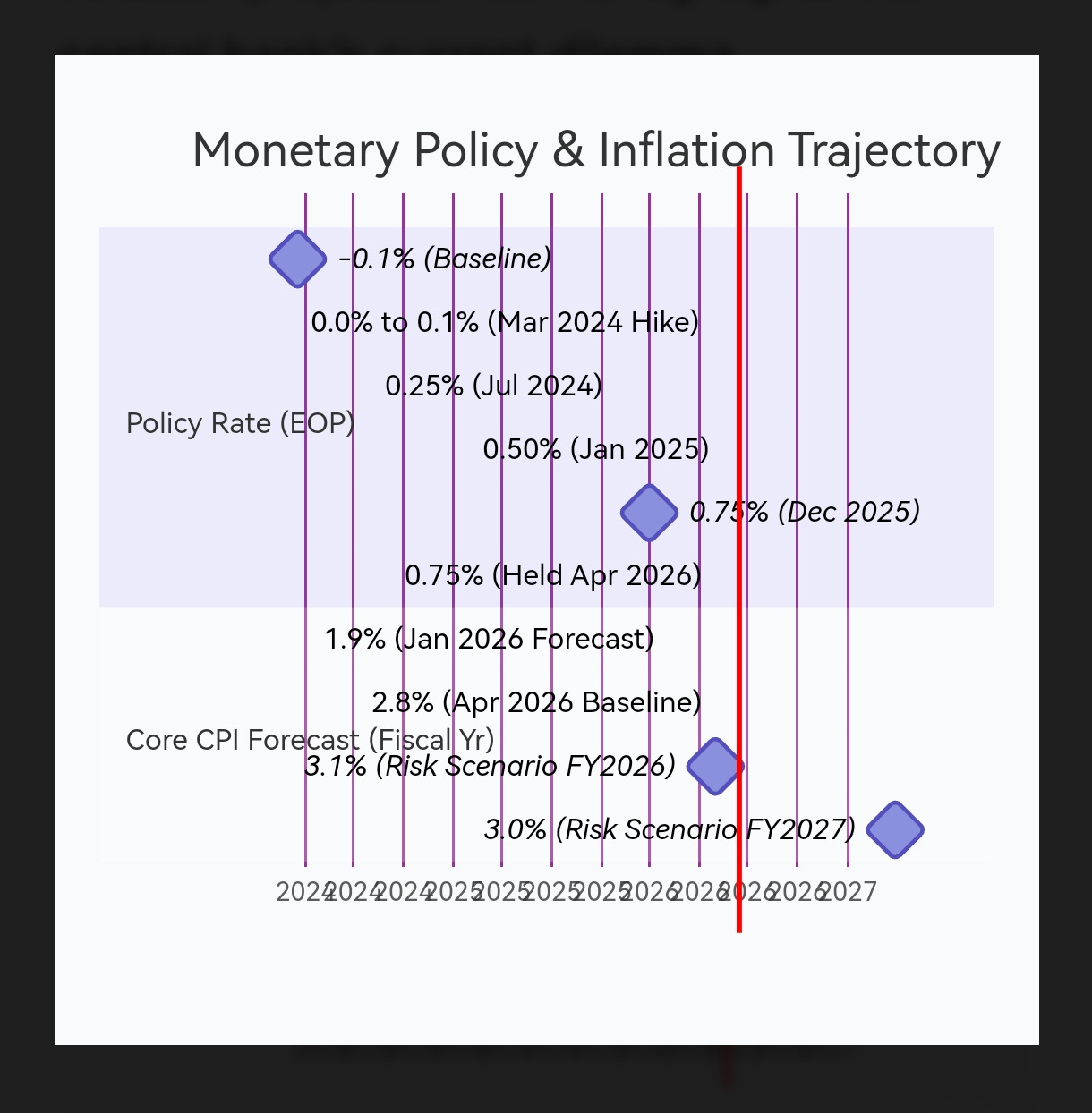

Figure 1: Policy Rate Path and Inflation (2024–2026)

This chart shows the steady ascent of the BoJ’s policy rate from negative territory to 0.75 per cent, alongside the sharp upward revision to inflation forecasts driven by energy costs. The divergence between the actual rate (0.75%) and the risk-scenario inflation projection (3.1%) highlights the central bank’s current dilemma

( Data sources: BoJ Outlook Reports, April 2026; Reuters (5) )

The balance sheet presents an even more complex challenge than the policy rate. Having spent years acquiring Japanese government bonds, exchange-traded funds and corporate debt, the BoJ’s holdings ballooned to a scale that dwarfs any comparable institution. By mid‑2026, the current account balances held at the central bank stood at approximately 518 trillion yen, a figure equivalent to more than ninety per cent of Japan’s gross domestic product (2). The gradual reduction of this mountain has begun, with the BoJ slowing its monthly bond purchases from 2.9 trillion yen in early 2025 to 2.1 trillion yen by the first quarter of 2027, a pace that officials hope will reduce total holdings to somewhere between 200 trillion and 300 trillion yen over the medium term (7). Yet internal simulations reveal the narrowness of the path forward: maintaining the current tapering pace of 200 billion yen per quarter would see holdings drop to about 200 trillion yen, a level officials consider manageable, whereas a faster reduction to 100 trillion yen would almost certainly provoke severe volatility in the bond market (2). The BoJ finds itself in the unusual position of hoping that private banks continue to hold excess reserves at the central bank, as the alternative, those reserves being deployed into government bonds and driving yields sharply higher, represents a political nightmare for a finance ministry already servicing a national debt well above 250 per cent of GDP.

External observers, particularly at the United States Federal Reserve and the European Central Bank, watch this process with a mixture of sympathy and anxiety. The Fed raised rates aggressively in 2022 and 2023, then began shrinking its balance sheet through quantitative tightening, all while the dollar remained the world’s reserve currency and Treasury markets remained deep enough to absorb sales. The BoJ enjoys no such luxury. The Japanese government bond market, for all its size, has been so thoroughly dominated by the central bank for so long that trading volumes and price discovery have atrophied (6). When the BoJ abandoned its rigid cap on ten‑year yields in late 2023, replacing it with a more flexible reference point, the resulting volatility spread quickly across global fixed income, reminding investors just how interconnected these markets have become. Any misstep in Tokyo now carries consequences for bond yields in London and Sydney, given the vast holdings of Japanese investors in overseas sovereign debt.

The economic data offers contradictory signals about the wisdom of further tightening. On the one hand, the headline inflation rate has exceeded the BoJ’s two per cent target consistently for two years, and the labour market has tightened to levels not seen since the late 1980s. On the other hand, real wages remain under pressure, and the central bank’s own forecasts for economic growth in fiscal 2026 have been halved to just 0.5 per cent, a dramatic downward revision that reflects both the energy shock and weakening global demand (3). Household spending, the engine of any sustainable recovery, has failed to accelerate in a convincing manner, suggesting that Japanese consumers remain trapped in the deflationary mindset that three decades of low prices instilled. If people believe prices will rise only moderately, and if wage increases are eaten up immediately by higher energy and food costs, then the virtuous cycle that Ueda described remains more theoretical than real.

Opposing voices within the BoJ’s own policy board have grown louder as inflation has proved stickier than anticipated. Some members argue that the bank has fallen behind the curve, pointing to the risk scenario analysis published in April 2026 which warned that core inflation could reach 3.1 per cent in fiscal 2026 and remain near three per cent the following year if oil prices stay elevated and the yen continues to weaken (5). Under this scenario, the BoJ would be forced to raise rates more aggressively later, potentially triggering a sharper economic slowdown than the gradual path would produce. The counterargument, advanced by Ueda and the majority of board members, rests on historical memory. Japan attempted to raise rates in 2000 and again in 2006, only to see those efforts derailed by external shocks and weak domestic conditions. The current normalisation is proceeding at a pace designed to ensure that if it fails, it fails slowly and with minimal financial disruption, a defensive posture that reflects the trauma of past policy mistakes rather than confidence in present economic strength.

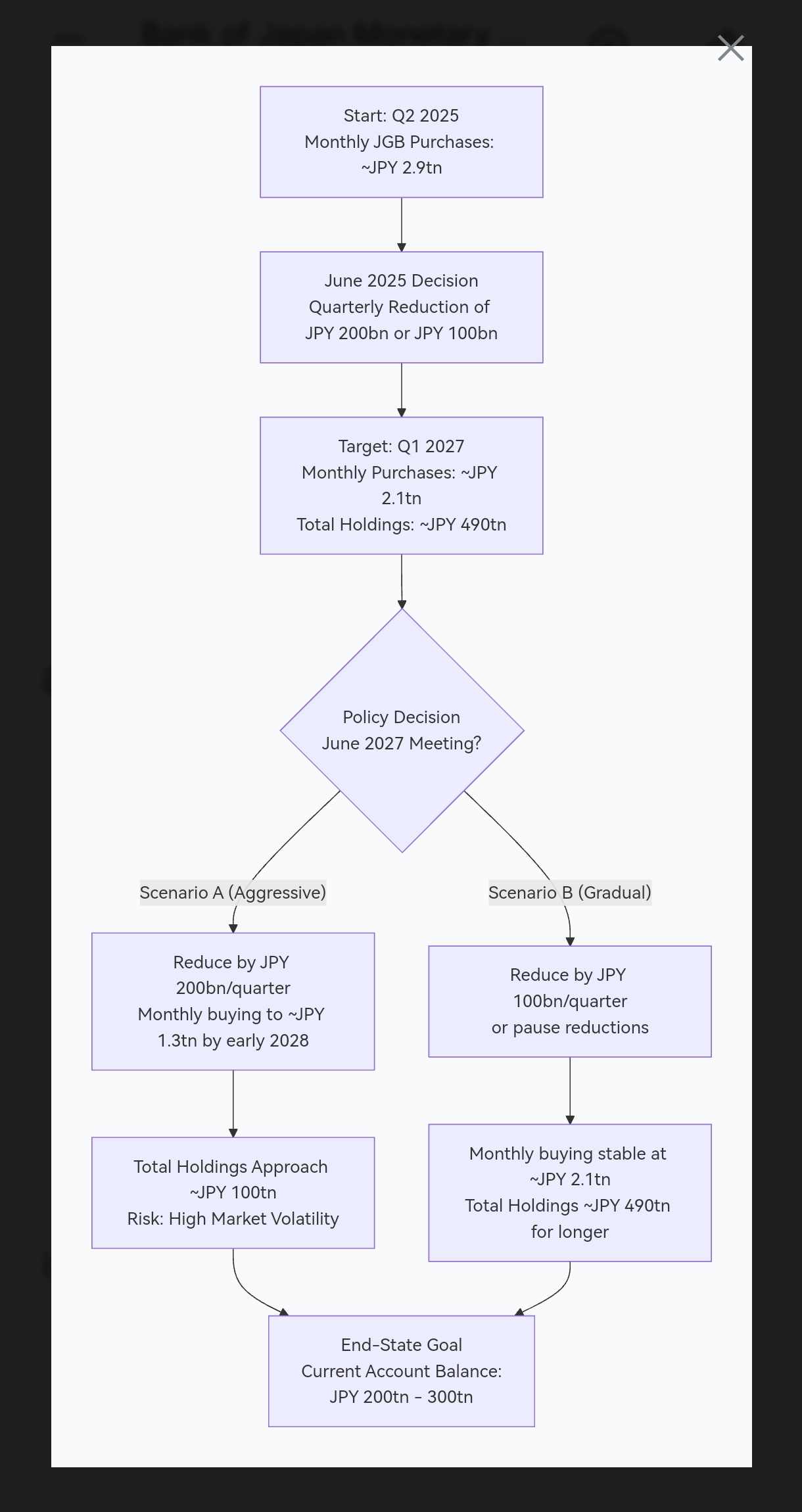

Figure 2: The Balance Sheet Reduction Roadmap (2026–2028)

The diagram below visualises the BoJ’s planned reduction in monthly Japanese Government Bond (JGB) purchases and the corresponding decline in total holdings. The central bank faces a strategic choice between a gradual taper (JPY 200bn quarterly reduction) and a more aggressive path, with officials viewing the latter as likely to cause excessive market volatility.

(Data sources: MNI Policy analysis, 2026 (2 ; 7); BoJ statements.)

The political dimension of this transition cannot be separated from the economic mechanics. Prime Minister’s office has maintained a careful public silence on monetary policy, respecting the central bank’s formal independence, but behind the scenes the finance ministry has made its preferences abundantly clear. Higher interest rates directly increase the cost of servicing Japan’s enormous public debt, eating into a budget already strained by rising defence spending and social security costs for an ageing population. Every one percentage point increase in the average interest rate on government bonds adds roughly ten trillion yen to annual debt service costs, a sum larger than the entire education budget. The BoJ’s bond holdings, however, provide a partial offset, as interest payments made by the government to the central bank are largely returned to the treasury. This circular flow means that the net fiscal impact of rate normalisation is considerably smaller than headline numbers suggest, a technical detail that Ueda has used to deflect political pressure while maintaining his gradual approach.

Looking toward the remainder of 2026 and into 2027, the BoJ faces three interconnected decisions that will define its legacy. First, the policy rate must eventually move above one per cent if the bank is to regain any meaningful ability to cut rates during the next recession, but the timing of such a move remains contingent on wage data that will not be clear until the spring negotiations of 2027. Second, the pace of balance sheet reduction will need to accelerate or slow depending on how private banks absorb the bonds the BoJ is no longer buying; early 2027 will see a quarterly reduction decision that may cut purchases by either 100 billion or 200 billion yen, a choice that carries significant implications for long‑term yields (7). Third, and most critically, the BoJ must decide whether to treat the current energy‑driven inflation as a justification for further tightening or as an external disturbance that will fade on its own. This last question has split monetary policy committees across the developed world, but for Japan, where imported inflation collides with stagnant domestic demand, the answer is particularly elusive.

Governor Ueda has repeatedly characterised the current process as feeling the way toward an appropriate balance sheet level, a phrase that captures both the uncertainty and the seriousness of the undertaking (2). The BoJ is navigating waters that no central bank has charted before, attempting to exit a monetary regime so extreme that it was once dismissed as impossible to reverse. The disappearance of negative interest rates and the slow retreat from bond markets represent genuine achievements, proof that the Japanese economy can function without the extraordinary support it has required for fifteen years. But the final chapter of this story remains unwritten, and the risk of a policy misstep, whether through excessive haste or damaging delay, hangs over every decision. The Bank of Japan has begun its long goodbye to unconventional policy, but the farewell may take years to complete, and the audience, consisting of Japanese households, global investors, and the entire central banking community, remains rightly uncertain about how the performance will end.

Authored By: Global GeoPolitics

If you prefer to make a one time donation in support of my work, you can do so by clicking any link below:

https://buymeacoffee.com/ggtv |

https://ko-fi.com/globalgeopolitics |

Bitcoin: 3NiK8BoRZnkwJSHZSekuXKFizGPopkE7ns

References

- Thorbecke, W. (2026, May). How is Policy Normalization by the Bank of Japan Affecting the Link between Monetary Policy and Stock Prices. Research Institute of Economy, Trade and Industry (RIETI). -1

- Inoue, H. (2026, July 18). MNI POLICY: BOJ To Feel Way To Appropriate Balance Sheet Level. MNI Market News. -2

- Bank of Japan hikes inflation forecast, holds interest rates. (2026, April 28). Bangladesh Sangbad Sangstha (BSS) / AFP. -3

- Yamaguchi, M. (2024, March 19). The Bank of Japan ends its negative interest rate policy, opting for its first hike in 17 years. Associated Press. -4

- Kihara, L. (2026, April 30). BOJ warns inflation could rise well above target in risk scenario. Reuters. -5

- 摩通:日本央行調整孳息曲線控制政策 日本股、滙波動. (2023, July 28). Hong Kong Economic Journal. -6

- Inoue, H. (2026, February 20). MNI POLICY: BOJ To Eye JGB Buying Cut To Lower Balance Sheet. MNI Market News. -7

- Ergöçün, G. (2026, April 28). Bank of Japan keeps policy rate constant. Anadolu Agency. -8

- Ma, T. (2024, March 19). Japan: The end of NIRP and YCC. DBS Bank Group Research. -9

- The Bank of Japan kept interest rates unchanged at 0.75%, raising its inflation forecast to 2.8%. (2026, April 28). Vietnam.vn. -10

Leave a comment