How America’s first bank failure of 2026 was buried as silver broke, markets fell, and war decisions stalled

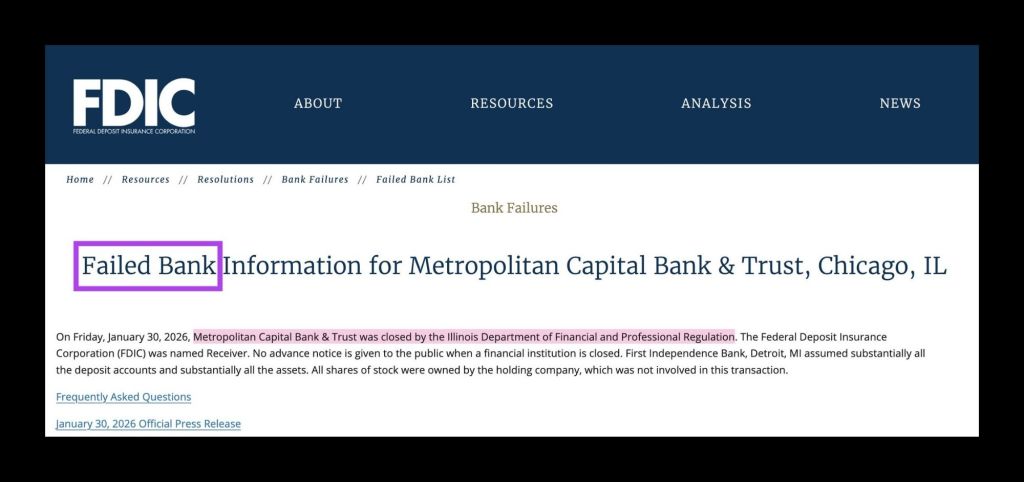

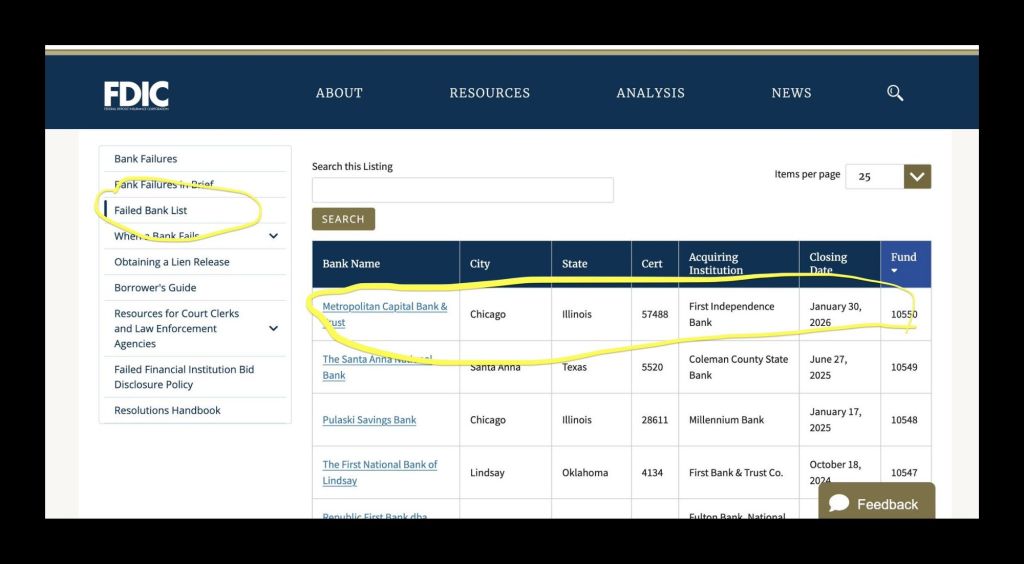

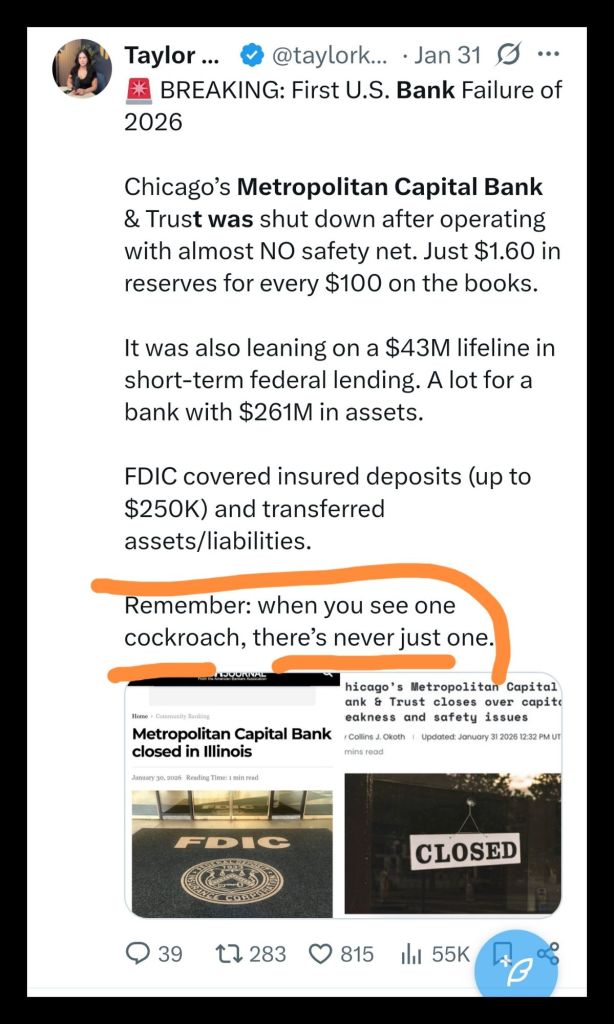

The first United States bank failure of 2026 occurred without public disorder, market panic, or sustained media attention, reflecting a deliberate administrative approach shaped by post-2008 regulatory practice, an approach described by former Federal Reserve official Daniel Tarullo as resolution through “operational continuity over public disclosure”. Illinois regulators closed Metropolitan Capital Bank and Trust on a Friday, transferring operations through a managed resolution that preserved depositor access and maintained routine loan obligations, consistent with what Columbia University economist Adam Tooze has described as crisis management designed to “remove the theatre of collapse from public view”.

Deposits remained accessible throughout the process, with regulators stating clearly that all customer accounts would function without interruption under federal insurance arrangements, echoing the deposit assurance doctrine articulated by Mervyn King during the post-crisis reforms of the Bank of England. The institution held approximately two hundred and sixty-one million dollars in assets at the time of closure, placing it firmly within the category of small regional banks vulnerable to tightening credit conditions, a vulnerability long documented by Hyman Minsky’s financial instability hypothesis. The bank failure followed a well-worn post-2008 resolution framework designed to prevent visible collapse while absorbing losses quietly through regulatory channels, reflecting what Harvard Law professor Hal Scott defined as “containment without illumination”. Federal and state authorities avoided press conferences or emergency announcements, limiting public exposure to the event and reducing the likelihood of depositor contagion, a strategy consistent with the crisis communication restraint advocated by former IMF economist Desmond Lachman.

Chicago’s long history of bank failures provided institutional memory for this approach, with regulators drawing on past regional collapses to shape the 2026 response, a pattern documented by University of Chicago banking historian Charles Calomiris. Metropolitan Capital Bank did not experience a disorderly run, reflecting careful coordination between Illinois regulators and the Federal Deposit Insurance Corporation, an outcome aligned with Sheila Bair’s earlier assertion that “runs are prevented administratively, not rhetorically”.

The FDIC moved rapidly, assuming control and arranging a managed handoff that prevented immediate spill-over effects into neighbouring institutions, a process that regulators themselves described as fully prepared rather than reactive. Officials described the process as a controlled resolution rather than a systemic emergency, emphasising preparedness rather than improvisation, language consistent with post-crisis supervisory manuals developed under Basel III frameworks. This method aligned with regulatory theory developed after the global financial crisis, where individual institutional failures are resolved discretely to preserve system confidence, a principle outlined by economist Anat Admati in her work on bank capital resilience.

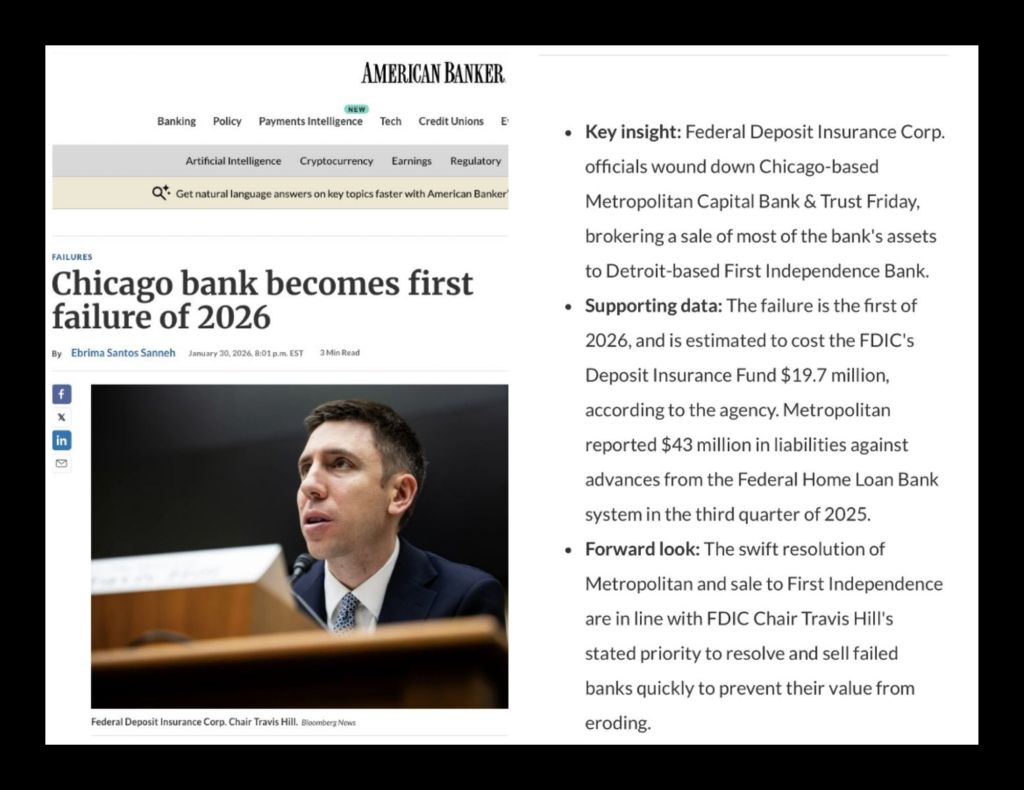

The closure occurred amid tightening financial conditions, with smaller banks facing disproportionate stress as liquidity retreated from peripheral institutions, a phenomenon described by former BIS chief economist Claudio Borio as late-cycle balance sheet compression. Rising funding costs and declining asset valuations had already placed pressure on regional balance sheets before the failure occurred, reflecting the transmission mechanisms outlined in Irving Fisher’s debt-deflation theory. The Metropolitan Capital collapse therefore functioned as a signal rather than an anomaly, reflecting structural fragilities rather than isolated mismanagement, a distinction emphasised by economic historian Niall Ferguson in his analysis of financial cycles. Regulators acknowledged that such failures carry symbolic weight, even when operational disruption remains limited through administrative control, a view shared by sociologist Wolfgang Streeck regarding legitimacy erosion in late-stage financial systems.

The economic context surrounding the failure included declining equity markets, falling cryptocurrency valuations, and sharp movements in commodity pricing, developments consistent with cross-asset deleveraging described by analyst Michael Hudson. At the same time, the Chicago Mercantile Exchange experienced a severe dislocation in the silver market, marked by abrupt price declines and contract instability. The silver crash coincided with declining gold prices, undermining traditional hedging strategies relied upon during periods of geopolitical and financial uncertainty, an outcome warned about by metals analyst Alasdair Macleod in his critiques of futures market leverage. Independent commodities analysts noted that forced liquidation and margin pressure, rather than physical supply conditions, drove the rapid collapse in precious metals pricing, echoing arguments advanced by the CPM Group and veteran trader Andrew Maguire. This market event occurred without coordinated public explanation from exchange authorities, mirroring the communication restraint observed during the bank resolution.

The concurrent decline in cryptocurrencies reflected broader liquidity withdrawal, as leveraged participants exited positions across risk and alternative asset classes, consistent with Nouriel Roubini’s assessment of speculative asset sensitivity to monetary tightening. Stock markets followed a similar downward trajectory, with regional banking exposure amplifying losses in financial sector indices. This pattern aligned with observations by heterodox monetary economists who argue that modern financial stress emerges first through liquidity contraction rather than headline defaults, a view long held by Steve Keen. Such dynamics echo the slow-motion stress test described by regulatory observers, where weak institutions are resolved individually instead of collapsing simultaneously.

Geopolitically, the bank failure and commodity market disruption unfolded during ongoing regime-change conflicts and heightened strategic tension in the Middle East. Policy deliberations regarding military action against Iran remained unresolved during this period, with financial instability constraining escalation timelines, a linkage examined by realist scholars such as Glen Diesen. Strategic analysts have long noted that major military operations depend on stable financial conditions to sustain supply chains and fiscal credibility, a principle articulated by historian Paul Kennedy in his work on imperial overstretch. Delayed decision-making reflected concerns that market volatility could undermine domestic economic stability during a period of elevated geopolitical risk.

The absence of media amplification surrounding the bank failure contrasted sharply with earlier crises, reflecting evolved information management strategies. Officials appeared focused on maintaining public calm rather than framing the event as evidence of systemic fragility, a posture described by former central banker Willem Buiter as “stability through silence”. This approach aligned with post-crisis regulatory philosophy prioritising perception management alongside balance sheet repair. Critics of this model argue that quiet resolutions obscure underlying structural weaknesses, delaying necessary political and financial reform, a critique advanced by economist Richard Werner. Supporters counter that visible panic inflicts greater damage than discreet administrative intervention during periods of economic strain.

Historical precedent supports both interpretations, with past crises demonstrating that suppression of panic can stabilise markets temporarily while compounding longer-term risks. The 2008 financial crisis illustrated how delayed recognition of systemic insolvency magnified eventual economic and social costs. Conversely, uncontrolled bank runs during earlier twentieth-century crises produced immediate economic contraction and political instability. The 2026 response reflected lessons drawn selectively from these episodes, favouring administrative containment over public confrontation.

Metropolitan Capital Bank’s closure therefore represented more than a local institutional failure, serving instead as an indicator of broader systemic adjustment. The simultaneous disruption of precious metals markets and alternative assets suggested coordinated deleveraging across the global financial system. These developments occurred within a fragile geopolitical environment where economic resilience underpinned strategic decision-making. Quiet management prevented immediate crisis escalation but left unresolved questions regarding underlying financial sustainability.

Authored By: Global GeoPolitics

Thank you for visiting. This is a reader-supported publication. I cannot do this without your support. You can support by way of a cup of coffee:

buymeacoffee.com/ggtv or

Leave a reply to The Bulletin: January 28-February 3, 2026 – Olduvai.ca Cancel reply