Strait of Hormuz disruption, sanctions blowback, and energy market chaos exposing the fragility of globalisation and accelerating geopolitical realignment

Economic history repeatedly demonstrates the law of unintended consequences operating with particular force during military escalation and coercive sanctions regimes. The confrontation surrounding Iran now produces cascading disruptions across energy markets, alliances, shipping networks, and domestic political systems. Strategic consequences appear uneven because global energy supply remains concentrated within narrow maritime corridors and a small number of producing states.

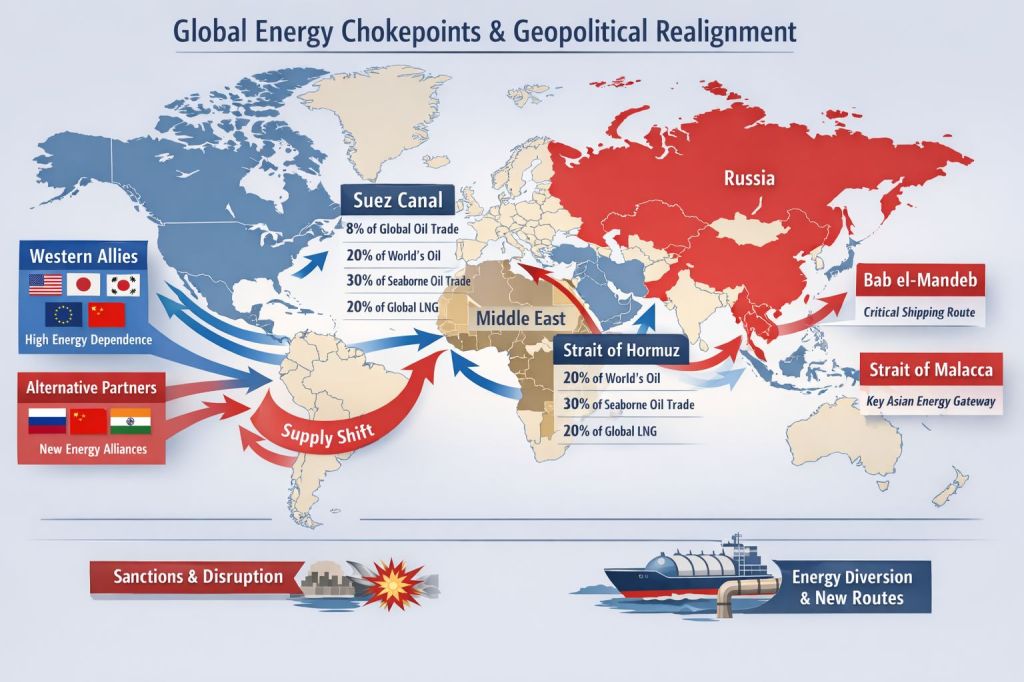

Roughly twenty to twenty one million barrels of crude oil and petroleum products transit the Strait of Hormuz each day, representing approximately thirty percent of global seaborne petroleum trade and roughly one fifth of total global petroleum consumption (U.S. Energy Information Administration). Annual cargo value moving through that narrow waterway approaches one point two trillion dollars under normal price conditions (Ballast Markets analysis). Liquefied natural gas shipments also depend heavily upon that corridor, with approximately twenty percent of global LNG trade moving through the same passage (International Energy Agency LNG trade data). Asian markets absorb more than eighty percent of the hydrocarbons travelling through that chokepoint, producing a structural vulnerability across the industrial economies of East Asia (Energy Information Administration shipping analysis).

Military confrontation surrounding Iran therefore produces immediate strategic consequences for energy dependent manufacturing economies. South Korea imports approximately seventy percent of its crude oil from Middle Eastern producers, while significant volumes move through Hormuz before reaching Korean refineries (Reuters energy market reporting). Japanese energy dependence appears even greater because roughly ninety five percent of Japanese crude imports originate from Middle Eastern exporters (International Energy Agency country profile). Approximately seventy percent of those Japanese imports pass directly through the Strait of Hormuz, creating a structural exposure embedded within Japanese industrial production (U.S. Energy Information Administration). South Korea and Japan both maintain strategic petroleum reserves approaching two hundred days consumption, although reserve drawdowns cannot permanently substitute for interrupted maritime supply (International Energy Agency emergency oil stockholding data).

Shipping disruption quickly demonstrates how narrow logistical bottlenecks translate into systemic global consequences. Commercial traffic through the Strait reportedly collapsed by roughly ninety four percent during the early phase of escalation, falling from around one hundred thirty eight vessels daily to approximately eight transits (MarketWatch shipping analysis). Energy markets reacted immediately, producing crude price increases approaching thirty percent within a single week of hostilities (Reuters commodities reporting). Nearly fifteen million barrels per day of crude oil and an additional four point five million barrels per day of refined petroleum products suddenly became stranded behind the disrupted maritime corridor (Reuters energy market analysis). Energy traders simultaneously reported Asian liquefied natural gas prices nearly doubling during the same early conflict period (Financial Times energy market coverage).

Taiwan faces a separate but related vulnerability rooted in limited liquefied natural gas storage capacity. Japanese authorities publicly state that LNG inventories within Japan cover roughly three weeks of domestic demand, illustrating how limited storage capacity remains common across highly industrialised energy importers (Japan Ministry of Economy Trade and Industry energy reports). Taiwanese planners therefore consider coal fired generation as emergency backup because LNG supply interruptions threaten electrical grid stability within weeks.

Energy dependency patterns across Asia reveal why strategic planners monitor the Strait of Hormuz with unusual attention. China imports approximately three point eight million barrels of crude oil daily through the strait, representing roughly thirty percent of Chinese oil imports (Visual Capitalist global oil flows). India receives roughly two million barrels per day through the same route, while Japan and South Korea each import roughly one point six to one point seven million barrels daily through the corridor (Energy Information Administration global flows dataset). China nevertheless maintains a comparatively stronger buffer because domestic production exceeds four million barrels daily and strategic reserves reportedly exceed nine hundred million barrels (Reuters energy reserves reporting). Long term stockpiling and diversified supplier relationships with Russia and Latin American producers therefore moderate Chinese vulnerability relative to neighbouring economies.

Economic consequences extend beyond energy markets because global shipping networks depend heavily upon predictable maritime corridors. Insurance premiums for vessels entering the Persian Gulf increased sharply while major shipping companies reroute vessels around the Cape of Good Hope or delay voyages entirely (Lloyd’s maritime risk analysis). Logistics disruptions increase freight costs and delivery times across industrial supply chains already strained by geopolitical fragmentation.

Political consequences appear equally visible across allied states closely associated with American military deployments. Australian public debate intensifies because United States military basing arrangements across northern Australia increasingly appear as potential strategic targets during regional conflict (Australian Strategic Policy Institute analysis). Foreign residents departing Dubai through overcrowded outbound flights illustrate how financial centres integrated within global tourism networks experience rapid capital and population flight during wartime uncertainty (regional aviation and travel industry reporting).

Diplomatic embarrassment surrounding United States energy policy toward India illustrates further unintended consequences produced by sanctions regimes. Washington publicly granted India permission to purchase Russian crude oil despite the widely known reality that New Delhi never halted those imports (Reuters sanctions coverage). India imports roughly fifty five percent of its crude oil from Middle Eastern producers while also maintaining extensive purchasing arrangements with Russia following the Ukraine conflict (International Energy Agency oil market statistics). Russian energy exporters consequently receive increasing purchase enquiries from states seeking alternative supply arrangements beyond Western sanction frameworks.

Vladimir Putin “thinking out loud” about rerouting Russian gas supplies from Europe. “Now other markets are opening up – perhaps it would be more profitable for us to stop supplying Europe and move to new markets and gain a foothold there. I want to be clear, there is no political subtext here”

Western sanctions against Russian energy exports during the Ukraine conflict aimed to isolate Moscow economically and collapse fiscal capacity supporting its military operations. European Union governments simultaneously announced a phased strategy terminating dependence upon Russian pipeline gas before the year 2027 (European Commission energy strategy). European gas imports from Russia previously exceeded one hundred fifty billion cubic metres annually before the sanctions regime and pipeline disruptions began restructuring continental supply chains (Eurostat gas import statistics).

Energy market pressures now produce a reversal of earlier political language within Washington. American officials quietly consider easing restrictions on Russian crude sales in order to stabilise international oil prices following escalation surrounding Iran and the Strait of Hormuz (Reuters policy reporting). Washington already acknowledged practical limitations of its sanctions regime by formally permitting India to continue purchasing Russian crude oil despite previous attempts to restrict such trade (U.S. Treasury sanctions statements).

Russian energy exports adapted rapidly during the past three years by redirecting flows toward Asian markets. Russian crude deliveries to India increased from negligible volumes before 2022 to more than one point five million barrels per day during recent trading periods (International Energy Agency Oil Market Report). Chinese refiners simultaneously expanded purchases through long term supply agreements and discounted pricing structures attractive to large importers seeking alternatives to Middle Eastern supply (Chinese customs trade data analysis).

President Vladimir Putin recently indicated that Moscow may terminate remaining pipeline gas deliveries to Europe before the European Union’s own 2027 diversification deadline (Kremlin energy policy statements). Russian officials openly state that gas volumes previously directed toward European markets can increasingly flow toward Asian consumers through expanding pipeline infrastructure and liquefied natural gas export capacity (Gazprom export strategy releases). Russian government representatives also emphasise that states maintaining cooperative relations with Moscow will receive favourable commercial arrangements during future supply negotiations.

Hungary and Slovakia already maintain relatively stable access to Russian pipeline gas under exemptions negotiated within European sanction frameworks (European Commission documentation). Governments in Budapest and Bratislava therefore experience lower wholesale gas prices compared with several Western European states forced to replace pipeline imports with more expensive liquefied natural gas shipments arriving through maritime terminals (Eurostat energy price statistics).

European industrial competitiveness consequently deteriorated during the past two years as natural gas prices increased several hundred percent above historical averages following the reduction of Russian pipeline supply (European Central Bank economic analysis). Energy intensive industries including fertiliser production, aluminium smelting, and chemical manufacturing reduced output or relocated capacity toward regions offering lower energy costs (European industry association reports).

Policy originally designed to isolate Russian energy exports therefore generated an unintended reconfiguration of global energy trade. Russian producers secured alternative markets while European industry confronted structural cost disadvantages associated with expensive imported liquefied natural gas. Strategic leverage once exercised through European dependence upon Russian pipeline gas therefore transformed into a wider global contest over energy pricing, transport infrastructure, and political alignment.

Strategic theory developed by Professor John Mearsheimer within offensive realism describes how states respond to perceived hegemonic pressure by constructing balancing coalitions designed to preserve strategic autonomy (Mearsheimer – The Tragedy of Great Power Politics). Professor Jeffrey Sachs similarly argues that sanction regimes and military encirclement accelerate geopolitical fragmentation because targeted states seek alternative economic networks outside Western financial systems (Jeffrey Sachs commentary at Columbia University). Norwegian political economist Glenn Diesen describes this process as the erosion of a unipolar order maintained through financial dominance, security alliances, and control of critical trade infrastructure (Diesen – Europe as the Western Peninsula of Greater Eurasia). Russian analyst Stanislav Kaprivnik and geopolitical writer Pepe Escobar describe globalisation during the post Cold War period as a system integrating peripheral economies into Western strategic networks through finance, trade institutions, and military security guarantees (Pepe Escobar geopolitical analysis).

Energy geography now exposes structural weaknesses within that architecture. Approximately eighty nine percent of crude oil moving through the Strait of Hormuz ultimately supplies Asian markets, while the United States itself receives only about two point five percent of that flow (Visual Capitalist energy trade dataset; Energy Information Administration).

Strategic vulnerability therefore concentrates within manufacturing economies dependent upon uninterrupted maritime imports rather than within the North American producer economy. Such asymmetry reshapes incentives across states forced to reconsider the reliability of alliance commitments during systemic supply shocks.

Game theory provides a structured framework for analysing behaviour emerging from such strategic uncertainty. Each state participating within the global energy market attempts to minimise vulnerability while maximising secure access to supply under conditions of incomplete information. Energy importers therefore diversify suppliers, accumulate reserves, and explore alternative transport corridors whenever geopolitical conflict threatens existing maritime routes. Energy exporters simultaneously seek new long term contracts with emerging markets prepared to bypass sanctions or political pressure from competing powers. Accumulated decisions across multiple actors gradually weaken centralised control structures previously sustained through military protection of trade routes and financial system leverage.

Law of unintended consequences therefore operates through the interaction of rational decisions by numerous states responding to shifting incentives under conflict conditions. Military escalation intended to reinforce strategic dominance instead accelerates energy diversification, trade rerouting, alliance reassessment, and financial system fragmentation across the international system.

Authored By: Global GeoPolitics

Thank you for visiting. If you believe journalism should serve the public, not the powerful, and you’re in a position to help, becoming a PAID SUBSCRIBER truly makes a difference. Alternatively you can support by way of a cup of coffee:

https://buymeacoffee.com/ggtv |

https://ko-fi.com/globalgeopolitics |

References

Ballast Markets. Strait of Hormuz Oil Chokepoint Analysis.

https://content.ballastmarkets.com/blog/2025-11-24-strait-hormuz-oil-chokepoint/

U.S. Energy Information Administration. Strait of Hormuz Oil Transit Data.

https://www.eia.gov/international/analysis/special-topics/Strait_of_Hormuz

Energy Analytics Institute. Around 20 Percent of Global LNG Trade Flows Through the Strait of Hormuz.

https://energy-analytics-institute.org/2025/06/24/around-20-of-global-lng-flows-through-strait-of-hormuz-eia/

Reuters. Iran War Threatens Global Energy Markets.

https://www.reuters.com/business/energy/iran-war-threatens-prolonged-hit-global-energy-markets-2026-03-07/

Financial Times. Global Energy Crisis and the Strait of Hormuz.

https://www.ft.com/content/5a74c0f8-1cf2-4a6b-9339-a098fcbeb100

MarketWatch. Oil Prices Surge Amid Strait of Hormuz Disruption.

https://www.marketwatch.com/story/oil-at-20-month-high-as-qatar-minister-warns-of-halt-to-energy-shipments-ffd3f8f9

European Commission. REPowerEU Energy Diversification Strategy.

https://energy.ec.europa.eu/topics/energy-security/repowereu_en

Eurostat. European Natural Gas Import Statistics.

https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Natural_gas_statistics

Mearsheimer, John. The Tragedy of Great Power Politics. University of Chicago Press.

Sachs, Jeffrey. Globalisation and the Geopolitics of Economic Sanctions. Columbia University Policy Papers.

Diesen, Glenn. Europe as the Western Peninsula of Greater Eurasia. Rowman & Littlefield.

Leave a comment