Energy disruption, inflation, rising debt costs, and global repricing of U.S. assets place sustained pressure across the entire economic system

A sharp break in United States financial markets during the final week of March 2026 raised the risk of a broader economic contraction extending beyond equities into the core functions of the economy and its global position. The removal of over two trillion dollars in market value between March 22nd and March 27th, combined with five consecutive weeks of losses, signalled more than a routine correction. The speed of the decline, the sectors affected, and the simultaneous stress in energy, labour, bond, and currency markets indicated that the disturbance carried implications for economic stability rather than temporary volatility.

Energy disruption formed the starting point of this shift. Escalation involving Iran restricted tanker movement through the Strait of Hormuz, a route responsible for a significant share of global oil supply. Brent crude prices rose above 108 dollars per barrel. Higher oil prices increased transport costs, raised production expenses for firms, and reduced disposable income for households. These pressures fed into inflation, preventing the decline in prices that financial markets had expected. Central banks could not reduce interest rates under these conditions without risking further inflation. Nouriel Roubini has described this dynamic clearly, noting that stagflation “locks policymakers into a position where any action worsens another part of the economy,” restricting effective response.

Stock markets had been rising on the assumption that interest rates would fall and liquidity would increase. When that assumption failed, valuations adjusted rapidly. Michael Howell of CrossBorder Capital has argued that asset prices in modern markets depend primarily on liquidity conditions rather than earnings growth. Once expected liquidity support disappeared, heavily valued sectors declined sharply. Technology firms such as Microsoft, Nvidia, and Meta led losses, with Microsoft alone accounting for a large share of weekly declines in major portfolios. The concentration of market value in a small number of firms meant that losses in those firms translated directly into broad index declines, a risk highlighted in Bank for International Settlements research on market concentration.

Market behaviour during this period showed that investor confidence had weakened. On March 22nd, a statement suggesting progress in negotiations with Iran added approximately two trillion dollars to the S&P 500 within one hour. When that statement was denied, one trillion dollars was lost shortly afterwards. Adam Tooze has explained that such movements occur when markets depend on policy signals rather than stable economic conditions. Investors were reacting to short-term political information because they no longer trusted long-term economic fundamentals to guide valuation.

Economic data confirmed that weakness extended beyond financial markets. The Institute for Supply Management services index fell close to contraction levels, indicating slowing activity in the largest part of the United States economy. Job losses increased across both private companies and government institutions. More than 172,000 corporate layoffs were announced in March, alongside over 280,000 public sector job cuts within two months. This reduced household income and spending capacity. Rising costs combined with falling employment created the conditions described as stagflation, where economic growth slows while prices continue to rise.

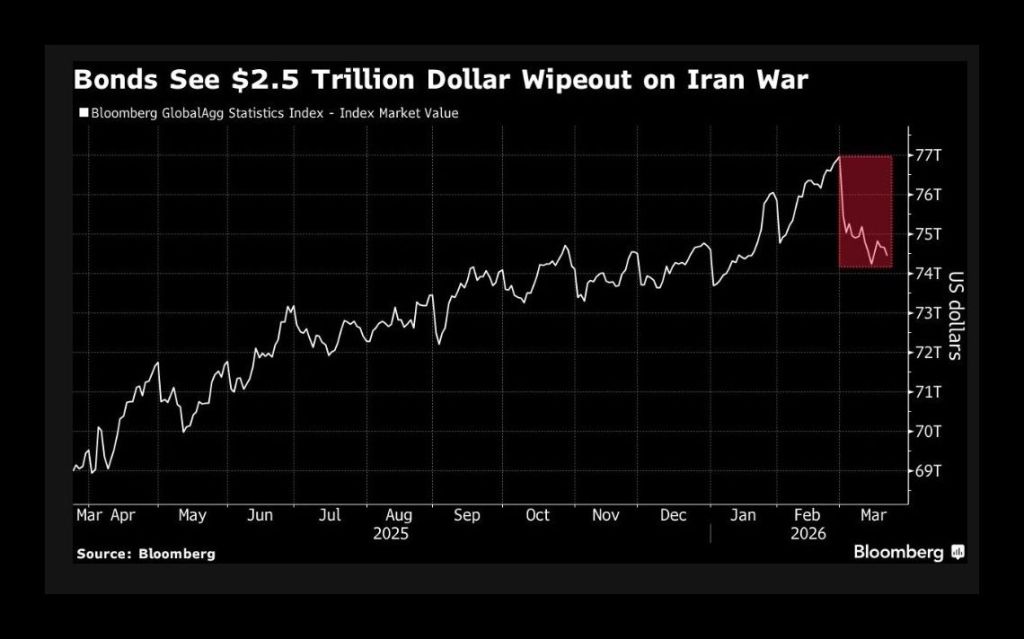

Bond markets provide a direct measure of how investors view government stability and risk. When governments borrow money, they issue bonds, which investors buy in exchange for regular interest payments. When demand for these bonds is strong, prices rise and yields fall. When investors lose confidence, they sell bonds or demand higher returns, causing yields to rise. During this period, yields on ten-year United States Treasury bonds rose to around 4.44 percent while stock markets were falling. Under normal conditions, investors move into these bonds during uncertainty because they are considered safe. The rise in yields showed that investors were not treating United States debt as a secure refuge. Zoltan Pozsar has argued that geopolitical changes and alternative financial systems are reducing automatic demand for United States debt, and this shift in bond market behaviour supports that analysis.

Currency movements reflect how investors view the strength of an economy relative to others. When confidence in a country’s economy weakens, investors move capital into other currencies, causing the original currency to fall in value. During this period, the euro and Canadian dollar strengthened against the United States dollar. This indicated that investors were diversifying away from dollar-based assets. Stephen Jen has written that such shifts occur when global investors begin to question the long-term stability of a dominant currency, particularly during periods of geopolitical fragmentation.

The situation therefore extended beyond falling stock prices. Higher energy costs increased inflation. Inflation prevented interest rate cuts. High interest rates raised borrowing costs for businesses and households. Job losses reduced income and spending. Rising bond yields increased the cost of government borrowing. Currency movements showed reduced global demand for dollar assets. Each of these developments affected different parts of the economy, but they reinforced each other rather than offsetting risk.

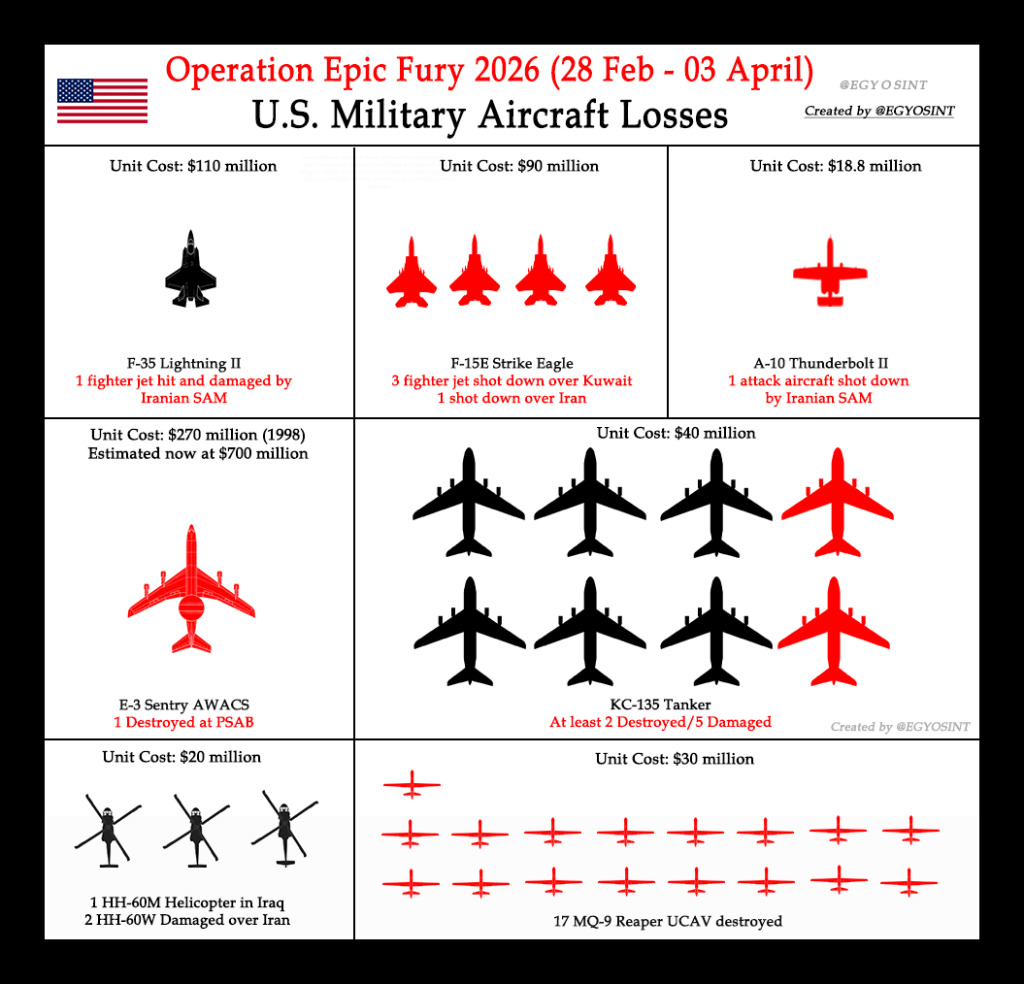

Geopolitical developments intensified these pressures. Military activity expanded in Lebanon, while tensions involving Iran remained unresolved. Incidents involving the deaths of United Nations peacekeepers in clearly marked positions showed that established rules governing conflict zones were weakening. Global trade and investment rely on predictable conditions and adherence to agreed rules. When those rules are disregarded, investors demand higher returns to compensate for increased risk or shift capital to more stable environments.

The global economy is directly exposed to these developments through several channels. Oil price increases affect production and transport costs worldwide. Changes in United States interest rates influence global borrowing costs, as many countries rely on dollar-denominated debt. Movements in the dollar affect trade balances and capital flows across emerging and developed markets. When confidence in United States financial assets weakens, global investors adjust portfolios, affecting liquidity across international markets. The United States financial system remains central to global finance, so instability within it transmits outward rather than remaining contained.

Developments after March 27th confirmed that these pressures continued. Oil prices remained elevated into early April, maintaining inflation. Stock markets experienced short-lived recoveries driven by political statements, though these did not reverse the overall decline. Bond yields remained high, showing continued pressure on government borrowing. Reports that United States Treasury officials sought additional foreign investment indicated concern about maintaining capital inflows, which are necessary to finance deficits.

A situation becomes economically catastrophic when several conditions occur at the same time and reinforce each other. These include sustained high energy prices, rising unemployment, falling asset values, increasing borrowing costs, and declining confidence in government debt and currency. During late March and early April 2026, all of these conditions were present simultaneously. If they continue without reversal, the likely outcomes include reduced economic growth, further market declines, constrained government spending, and pressure on the global financial system.

Current conditions show that the risk of a broader economic breakdown is no longer theoretical. Financial markets, government borrowing, household income, and international capital flows are all being affected at the same time. Subsequent developments have not corrected these pressures. They have confirmed that the underlying causes remain in place and continue to shape economic outcomes.

Authored By: Global GeoPolitics

Thank you for visiting. This is a reader-supported publication. If you believe journalism should serve the public, not the powerful, and you’re in a position to help, becoming a PAID SUBSCRIBER truly makes a difference. Alternatively you can support by way of a cup of coffee:

https://buymeacoffee.com/ggtv |

https://ko-fi.com/globalgeopolitics |

Bitcoin: 3NiK8BoRZnkwJSHZSekuXKFizGPopkE7ns

Leave a comment