How simultaneous chokepoint warfare has trapped global trade between two narrowing exits, a strategic game the West cannot easily exit

The Houthi declaration of entry into the war alters the structure of the conflict in a measurable way that can be tested against known data on maritime flows, energy dependency, escalation theory, and capital market transmission. Yemen’s position astride the Bab el-Mandeb creates leverage over a corridor that carried approximately 8.8 million barrels per day of crude and refined products according to the US Energy Information Administration’s 2024 assessment, alongside roughly one quarter of global container throughput. Combined with the Strait of Hormuz, where flows averaged between 17 and 21 million barrels per day, the present configuration places close to one third of seaborne oil trade under direct or indirect threat, a level of simultaneous exposure without precedent in modern energy system history.

Bassam Fattouh at the Oxford Institute for Energy Studies has shown that once disruption risk exceeds ten percent of global supply, oil markets shift into a different volatility regime rather than adjusting linearly. Current exposure surpasses that threshold on a gross basis and approaches it even on a net basis after partial rerouting. Independent trader Pierre Andurand has argued in investor letters during previous crises that price formation above $120 reflects scarcity pricing rather than marginal cost pricing, where small incremental disruptions produce outsized moves. Options markets already reflect this transition, with implied volatility exceeding 40 percent and skew favouring upside protection, a structure associated with tail risk rather than cyclical tightening.

The Houthis have demonstrated operational competence in maritime denial at scale. Lloyd’s List Intelligence recorded more than 120 interdiction attempts between 2023 and 2025, while insurance market data from the Joint War Committee showed war risk premiums on Red Sea routes increasing by more than 400 percent during peak periods. Fabian Hinz at the International Institute for Strategic Studies has documented the evolution of Houthi missile systems toward Iranian-derived platforms with ranges exceeding 1,000 kilometres and improved terminal guidance. This extends the threat envelope across the full width of the Red Sea choke and into approaches previously considered lower risk.

Cost asymmetry defines the engagement. CNAS estimates place the cost of one-way attack drones used by the Houthis between $20,000 and $50,000, while US Navy interceptor missiles range from $1.5 million to over $4 million per launch depending on system. Stacie Pettyjohn’s work on missile defence economics demonstrates that sustained engagements under such ratios erode defender capacity over time, particularly when the attacker retains initiative in timing and volume. A finite interceptor inventory combined with distributed launch platforms produces a structural advantage for the attacker even without achieving high hit rates.

Iran’s integration of the Houthis into a wider deterrence network reflects a doctrine analysed by Afshon Ostovar as forward defence through non-state actors, extending strategic depth and distributing retaliation capacity. Mohammad Marandi and other Iranian commentators have described this as a calibrated system designed to impose cumulative costs rather than decisive blows. The sequencing of Hormuz disruption followed by Houthi activation indicates coordination aimed at increasing marginal adjustment costs after initial adaptation pathways have been established.

The strategic interaction can be modelled as a sequential game with three principal players and multiple auxiliary actors. Iran’s first move constrains Hormuz, shifting global flows toward the Red Sea. The Houthis then threaten Bab el-Mandeb, increasing the cost of that shift. The United States must decide between escalation to reopen routes or acceptance of higher global costs. Israel operates within this framework but with independent targeting priorities. Payoff matrices favour Iran under conditions where disruption raises global prices without triggering full-scale retaliation. The United States faces higher marginal costs due to alliance commitments and domestic economic exposure, while non-state actors such as the Houthis incur comparatively low costs and therefore exhibit higher risk tolerance.

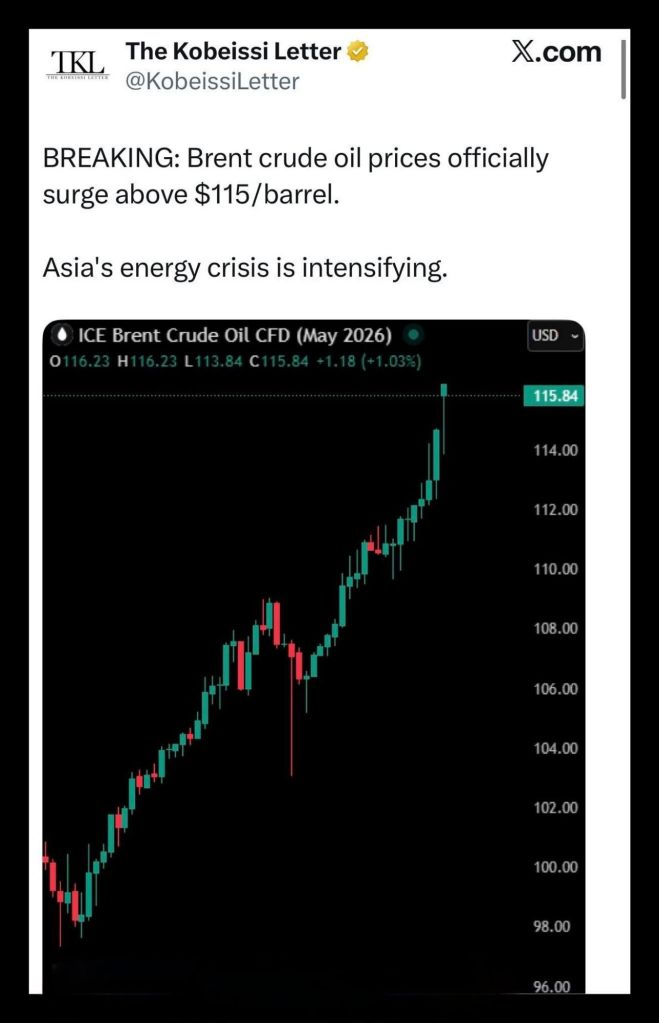

Energy market behaviour reflects this structure. Brent crude moved from approximately $70 to above $100 within four weeks, with forward curves entering backwardation consistent with immediate supply stress. Anas Alhajji has repeatedly argued that geopolitical premiums can add $20 to $40 per barrel independent of physical shortages, a range now visible in spread behaviour between prompt and deferred contracts. Fertiliser markets, linked to natural gas, show early signs of pass-through, with World Bank models indicating that sustained energy price increases translate into agricultural cost inflation within one to two quarters.

Shipping data confirms early-stage disruption. Clarksons Research recorded a reduction in Suez Canal transits of up to 40 percent during prior Houthi campaigns, with freight rates on Asia–Europe routes rising by more than 200 percent. Current conditions remove redundancy. Saudi Arabia’s East–West pipeline capacity of roughly 5 million barrels per day cannot compensate for Hormuz closure, and no equivalent bypass exists for Bab el-Mandeb. Routing around the Cape of Good Hope adds 10 to 15 days per voyage, increasing fuel consumption and tightening tanker availability, which in turn raises spot charter rates and feeds back into delivered energy prices.

Ukraine’s strikes on Russian energy infrastructure introduce a countervailing supply shock that tightens the system further. Satellite and tanker tracking data indicate that disruptions at Primorsk, Ust-Luga, and key refineries have removed between 1.5 and 2 million barrels per day of export capacity. Tatiana Mitrova has noted that Russia’s ability to reroute exports is constrained by port and pipeline infrastructure, limiting short-term elasticity. Before these strikes, higher global prices had already increased Russian revenue due to narrowing discounts. The removal of export capacity offsets that gain and reduces the buffering role Russian supply might otherwise play.

The interaction produces a compressed supply curve with high short-term price sensitivity. Rystad Energy estimates place OPEC spare capacity at around 4 to 5 million barrels per day, concentrated primarily in Saudi Arabia and the UAE, yet deployment of that capacity depends on secure export routes. If chokepoints remain contested, nominal spare capacity does not translate into effective supply. At the same time, prices above $120 historically trigger demand destruction in OECD economies within two quarters, as shown in International Energy Agency elasticity studies. The system therefore moves toward a potential overshoot, where short-term scarcity leads to medium-term contraction and eventual surplus once supply normalises.

Financial transmission channels amplify these dynamics. The Bank for International Settlements has quantified that a sustained $10 increase in oil prices adds roughly 0.4 percentage points to global inflation within a year. Rising inflation expectations influence central bank policy, increasing borrowing costs and tightening liquidity. Gulf sovereign wealth funds hold substantial allocations to US Treasuries, estimated through US Treasury International Capital data at several hundred billion dollars across Saudi Arabia, the UAE, and Kuwait. Signals from Iranian officials regarding targeting financial assets function as strategic messaging within what Adam Tooze describes as the financial dimension of modern conflict. Even marginal portfolio adjustments by large holders can affect yields in a high-debt environment where US fiscal deficits exceed $1.5 trillion annually.

Dissenting analysis from non-Western and independent observers sharpens the interpretation. Gulf-based maritime insurers have privately assessed that sustained Red Sea disruption beyond sixty days would force a structural repricing of shipping risk, not a temporary premium adjustment. Russian analysts such as Sergey Vakulenko have argued that Western assumptions about rapid restoration of supply routes underestimate the persistence of low-cost disruption. Iranian commentators frame the strategy explicitly as economic warfare designed to shift domestic political pressure within Western states rather than achieve battlefield victory. These perspectives converge on the expectation of prolonged disruption rather than short-lived shock.

The Yemen war provides empirical grounding for assessing regime resilience under sustained external pressure. The Saudi-led intervention beginning in 2015, supported by the United States, the United Kingdom, and other NATO-aligned states, aimed to restore the recognised government and degrade Houthi capabilities through airpower, blockade, and support for local proxies. Decapitation strategies were pursued repeatedly. Airstrikes targeted leadership structures, command nodes, and infrastructure. Despite these efforts, the Houthis consolidated control over northern Yemen, including the রাজধান capital Sanaa, and developed increasingly sophisticated missile and drone capabilities.

Academic studies by Farea Al-Muslimi and Michael Horton have documented how decentralised command structures and local legitimacy allowed the movement to absorb leadership losses without organisational collapse. The failure of decapitation strategies in Yemen aligns with broader findings in insurgency research, including work by Jenna Jordan, showing that leadership targeting rarely produces decisive outcomes against embedded movements with distributed authority.

The fragmentation of Yemen further illustrates limits of external intervention. The United Arab Emirates supported southern forces that eventually diverged from Saudi-backed factions, leading to the emergence of the Southern Transitional Council and effective partition of authority. Saudi influence weakened in key المناطق, while Emirati forces reduced their direct presence after sustaining costs without achieving strategic objectives. The net result involved neither restoration of the original government nor elimination of the Houthis, but a fractured landscape in which external powers failed to impose a stable outcome.

Parallels with Iran arise in the context of decapitation assumptions. Iran possesses a far more complex state structure, deeper institutional capacity, and larger population base than Yemen. Attempts to degrade leadership or infrastructure would encounter similar dynamics of redundancy and decentralisation, but on a larger scale. Afshon Ostovar and others have noted that the Islamic Republic has invested heavily in continuity planning and layered command structures precisely to mitigate such risks. The Yemen case provides a lower-bound estimate of resilience; Iran’s capacity likely exceeds it by a significant margin.

Game theoretic implications follow. Strategies premised on rapid collapse through leadership targeting carry low probability of success against actors with demonstrated resilience. Expected payoffs for such strategies decline further when adversaries possess escalation options affecting global economic systems. Iran’s ability to activate multiple nodes, including the Houthis, increases the cost of failure for opponents. The equilibrium shifts toward prolonged contestation rather than decisive victory.

Scenario analysis clarifies potential trajectories. A base case assumes partial disruption of both chokepoints, with oil prices stabilising between $110 and $140, elevated shipping costs, and gradual demand adjustment over six to nine months. An escalation case involves sustained closure or effective denial of both routes, pushing prices toward $150 to $200, triggering rapid demand destruction, financial tightening, and increased probability of coordinated intervention to restore flows. A systemic shock case combines chokepoint disruption with further loss of Russian supply or major infrastructure damage in the Gulf, producing extreme price spikes, severe recessionary pressure, and potential financial instability.

Trigger points include sustained interdiction rates exceeding insurance tolerance thresholds, depletion of interceptor inventories, direct strikes on major production facilities, or significant portfolio shifts by large sovereign holders of US debt. Monitoring these variables provides actionable signals for both policymakers and market participants.

The widening theatre therefore reflects structural incentives embedded in geography, technology, and financial interdependence. Maritime chokepoints provide leverage disproportionate to the resources required to contest them. Energy markets transmit local disruptions into global price signals. Financial systems incorporate geopolitical risk into asset valuation. Technological diffusion enables non-state actors to operate effectively within this system.

The Yemen precedent anchors the strategic conclusion. A coalition of advanced militaries failed over several years to dismantle a comparatively small, resource-constrained movement despite sustained air campaigns and leadership targeting. Internal divisions among coalition partners further reduced effectiveness. Iran presents a larger, more cohesive, and more strategically prepared adversary with integrated regional networks. Probability assessments based on empirical evidence from Yemen suggest that strategies aimed at rapid collapse through decapitation or external pressure face low likelihood of success and high risk of unintended escalation.

The present configuration therefore points toward a prolonged conflict defined by economic warfare, constrained escalation, and systemic volatility. Outcomes will depend on the capacity of each actor to absorb and impose cost across interconnected domains rather than on decisive military engagements alone.

The present configuration therefore points toward a prolonged conflict defined by economic warfare, constrained escalation, and systemic volatility. Outcomes will depend on the capacity of each actor to absorb and impose cost across interconnected domains rather than on decisive military engagements alone. The decisive variable shifts from force projection to endurance, where the side able to sustain economic disruption, infrastructure damage, and political strain over extended periods gains structural advantage. For Iran, the conflict carries an existential character tied to regime survival, which historically increases tolerance for sustained hardship, as seen during the Iran–Iraq War where prolonged attrition did not produce capitulation despite severe economic and human cost. By contrast, the United States and Israel operate within political and financial systems more sensitive to short-term economic dislocation, market instability, and domestic pressure, where sustained energy price shocks and supply chain disruption translate into immediate political cost.

Strategic doctrine emerging from Tehran reflects acceptance of short-term damage in exchange for long-term positional gain, a pattern consistent with analyses by scholars of revolutionary state behaviour who emphasise durability under sanction and isolation. The present escalation extends that logic into global economic systems, where imposed costs feed back into adversary societies. Historical precedent across declining or overextended powers suggests limits to such externalised pressure strategies. The experience of Saddam Hussein’s Iraq, which failed under combined military and economic strain despite regional ambitions, and broader cases of imperial overreach examined by historians such as Paul Kennedy, indicate that sustained multi-theatre commitments under economic stress erode strategic coherence over time. The current trajectory therefore carries a structural risk for the US-led coalition, where policies designed to impose short-term pressure may accumulate into longer-term strategic loss if endurance asymmetry remains unresolved.

Authored By: Global GeoPolitics

Thank you for visiting. This is a reader-supported publication. If you believe journalism should serve the public, not the powerful, and you’re in a position to help, becoming a PAID SUBSCRIBER truly makes a difference. Alternatively you can support by way of a cup of coffee:

https://buymeacoffee.com/ggtv |

https://ko-fi.com/globalgeopolitics |

Bitcoin: 3NiK8BoRZnkwJSHZSekuXKFizGPopkE7ns

References

Bassam Fattouh, “Oil Market Dynamics and the Role of Spare Capacity,” Oxford Institute for Energy Studies, various papers and reports, 2022–2024

Anas Alhajji, “Oil Markets, Geopolitics, and Price Formation,” independent energy analysis and commentary, 2023–2025

Pierre Andurand, Commodity Fund Letters and Investor Briefings, Andurand Capital Management, 2020–2025

Fabian Hinz, “Missile Proliferation and Non-State Actors in the Middle East,” International Institute for Strategic Studies (IISS), Strategic Dossiers, 2023–2025

Stacie L. Pettyjohn, “Cost Imposition and the Future of Air and Missile Defence,” Center for a New American Security (CNAS), 2021–2024

Afshon Ostovar, Vanguard of the Imam: Religion, Politics, and Iran’s Revolutionary Guards, Oxford University Press, updated analyses and lectures, 2016–2024

Mohammad Marandi, public lectures and policy commentary on Iranian strategic doctrine, University of Tehran, 2022–2025

Avinash K. Dixit and Barry J. Nalebuff, Thinking Strategically: The Competitive Edge in Business, Politics, and Everyday Life, W. W. Norton & Company

Thomas C. Schelling, The Strategy of Conflict, Harvard University Press

James D. Fearon, “Rationalist Explanations for War,” International Organization, Vol. 49, No. 3

Eugene Gholz, “Energy Vulnerability and Maritime Chokepoints,” University of Notre Dame, policy research papers, 2020–2024

Tatiana Mitrova, “Russian Energy Exports and Infrastructure Constraints,” Center on Global Energy Policy, Columbia University, 2022–2025

Rystad Energy, “Global Oil Supply, Spare Capacity, and Shale Breakeven Analysis,” Industry Reports, 2023–2025

International Energy Agency (IEA), “Oil Market Reports” and “Energy Security Analysis,” 2023–2025

World Bank, “Commodity Markets Outlook: Energy and Fertiliser Linkages,” 2023–2025

Bank for International Settlements (BIS), “Inflation Transmission and Commodity Price Shocks,” BIS Quarterly Review, 2022–2024

Adam Tooze, Crashed: How a Decade of Financial Crises Changed the World, and subsequent essays on financial warfare and geopolitical risk

Clarksons Research, “Shipping Intelligence Weekly” and Suez Canal transit data, 2023–2025

Lloyd’s List Intelligence and Joint War Committee, “Red Sea Risk Assessments and Maritime Insurance Premiums,” 2023–2025

Farea Al-Muslimi, “Yemen War Dynamics and Houthi Resilience,” Carnegie Middle East Center, 2019–2024

Michael Horton, “The War in Yemen and the Evolution of Houthi Power,” Jamestown Foundation and other policy publications, 2020–2024

Jenna Jordan, “Leadership Decapitation and Counterinsurgency Outcomes,” International Security, Vol. 36, No. 4

Sergey Vakulenko, Russian energy sector analysis and commentary, Carnegie Endowment and independent publications, 2022–2025

US Energy Information Administration (EIA), “World Oil Transit Chokepoints” and “Short-Term Energy Outlook,” 2023–2025

Kayrros, TankerTrackers.com, and satellite-based energy flow monitoring reports, 2024–2025

Hani Genena, “Macroeconomic Impact of Suez Canal Disruptions,” Cairo University and regional economic commentary, 2023–2025

Paul Kennedy, The Rise and Fall of the Great Powers, Yale University Press

Leave a comment