The CSRC Brokerage Crackdown, the Hong Kong Gold Clearing System, and the Euroclear Bond Integration – How Beijing Is Targeting the Financial Architecture That Makes Dollar Dominance Possible

The Iran ceasefire negotiations that have been publicly described since late April 2026 as approaching completion have not, as of the first days of June, produced a finalised agreement. The negotiating architecture as understood through Pakistani and Qatari mediators involves two principal elements: Iran’s reopening of the Strait of Hormuz on Iranian terms, in exchange for lifting the American naval blockade, followed at a later and unspecified date by an understanding on the dilution of Iran’s 60 percent enriched uranium stockpile in exchange for an end to sanctions. The gap between those two elements is not a technicality. Iran spent the war months establishing strategic dominance over a waterway through which one-fifth of the world’s seaborne oil transits, and it has demonstrated through the conduct of the conflict, striking thirteen American military bases, forcing the USS Gerald R. Ford from the Red Sea to Crete for repairs, shutting Ras Laffan and triggering the largest emergency oil reserve release in history, that it can impose costs the United States cannot absorb indefinitely without domestic political damage. Ali Akbar Velayati, Senior Adviser to Iran’s Supreme Leader, stated the Iranian position with the kind of geographic directness that the Trump administration’s dealmaking language tends to obscure: “The tangible guarantor of the agreement’s survival is the Strait of Hormuz. Geography does not lie, and it is the final judge over every covenant written on paper.” Tehran has no reason to surrender the leverage it earned at considerable cost for promises whose durability no American administration has demonstrated the institutional ability to maintain.

Trump’s dilemma in the ceasefire negotiations is, in the chess formulation that best describes it, zugzwang: any move available to him potentially worsens his position. A quick deal on Iranian terms, reopening Hormuz without securing a binding and verifiable nuclear agreement, draws immediate opposition from the pro-Israel donor class whose financial support defines the Republican Party’s operational capacity and whose pressure has already proven capable of breaking previous ceasefire attempts. When Trump’s earlier mooted arrangement appeared to lean toward an incomplete deal largely on Iranian terms, Israel responded by launching a renewed military assault on Lebanon and Gaza, breaching the ceasefire precondition that any settlement required, and forcing a resumption of conditions that made the deal politically untenable. Conversely, maintaining the naval blockade and prolonged Hormuz closure imposes mounting costs on the American economy, oil at above $90 per barrel, national average gasoline prices at $4.45 and rising, an inventory drawdown approaching operational minimums, and an Asian energy disruption that is fracturing the Indo-Pacific partnerships whose cultivation is supposed to be the war’s strategic compensation. Trump’s Beijing summit with Xi Jinping produced no major agreements and was characterised by images that Alastair Crooke, the former British diplomat and senior intelligence officer who served as EU Special Envoy for the Middle East, described as iconic: a US president wearing the air of defeat while a confident Xi’s comportment demonstrated who was in control of the encounter. The image, if it defines the era as Crooke suggested, defines it as one in which American presidential authority no longer commands the room in the way that American strategic planners had assumed it would when they designed the Iran campaign.

The financial dimension of the Iran war’s geopolitical consequences has received less analytical attention than the military and energy dimensions but may prove more durable in its effects. The United States Treasury’s strategy for sustaining dollar dominance in the post-petrodollar era has two principal legislative instruments: the GENIUS Act, signed into law by President Trump on 18 July 2025 following a 68-30 Senate vote and a 308-122 House vote, which established the first federal regulatory framework for dollar-backed payment stablecoins; and the Digital Asset Market Clarity Act of 2025, passed by the House with bipartisan support and awaiting Senate confirmation, which provides a complementary regulatory structure for non-stablecoin crypto assets. The combined architecture of these two statutes has a strategic function that extends well beyond domestic crypto market regulation. Dollar-backed stablecoins, by requiring their issuers to hold reserves primarily in short-term United States Treasuries, generate a structurally captive demand pool for American government debt. As Brookings Institution analysis confirmed in March 2026, stablecoin issuers can hold longer-dated Treasury securities as collateral for reverse repurchase agreements, meaning the demand for US debt generated through the stablecoin mechanism extends across the yield curve. The GENIUS Act’s reciprocity provision further requires the Federal Reserve, in collaboration with the Treasury Secretary, to create bilateral arrangements with overseas jurisdictions for interoperability with dollar-denominated stablecoins issued abroad, a mechanism for extending the dollar’s reach into overseas retail financial markets through crypto rails rather than the conventional petrodollar architecture that the Hormuz blockade has placed under observable strain. The strategic objective is to replace declining petrodollar demand for American Treasuries with crypto-dollar demand routed through overseas retail currency holders induced to exchange local currency positions for dollar-backed digital tokens.

China’s response to this financial architecture has not taken the form of sanctions or military counter-deployment. Beijing has instead applied what Crooke characterised as counter-pressure at the specific points of sensitivity within the American financial system, with a precision that reflects a sophisticated understanding of where dollar dominance is structurally vulnerable. On 22 May 2026, China’s Securities Regulatory Commission initiated enforcement actions against Tiger Brokers (New Zealand), Futu Securities International (Hong Kong), and Longbridge Securities (Hong Kong), the three dominant cross-border online brokerages through which mainland Chinese retail investors accessed American and international stock markets. The CSRC announced plans to eliminate their mainland operations entirely within two years, with Tiger Brokers and Futu facing combined fines of 2.3 billion yuan, approximately $330 million, and eight Chinese government agencies coordinating the enforcement campaign. An estimated $1 trillion in “hot money” had flowed out of China in 2025 seeking high-interest overseas assets, with the three firms together holding approximately $32 billion in assets under management for mainland clients. The South China Morning Post reported that mainland Chinese investors hold approximately HK$250 billion in assets through Hong Kong brokerage accounts with these firms. Wall Street, as TheStreet confirmed in analysis published 3 June 2026, depends on foreign buyers for a significant share of its equity market flows, and Chinese savings, at an estimated $50 trillion in bank deposits according to the World Economic Forum, exceeding the combined bank holdings of the EU, United States, and Japan, represent the largest single pool of potential foreign equity demand in the global financial system. Withdrawing that pool from American markets is a targeted financial pressure instrument whose magnitude dwarfs anything available through conventional sanctions.

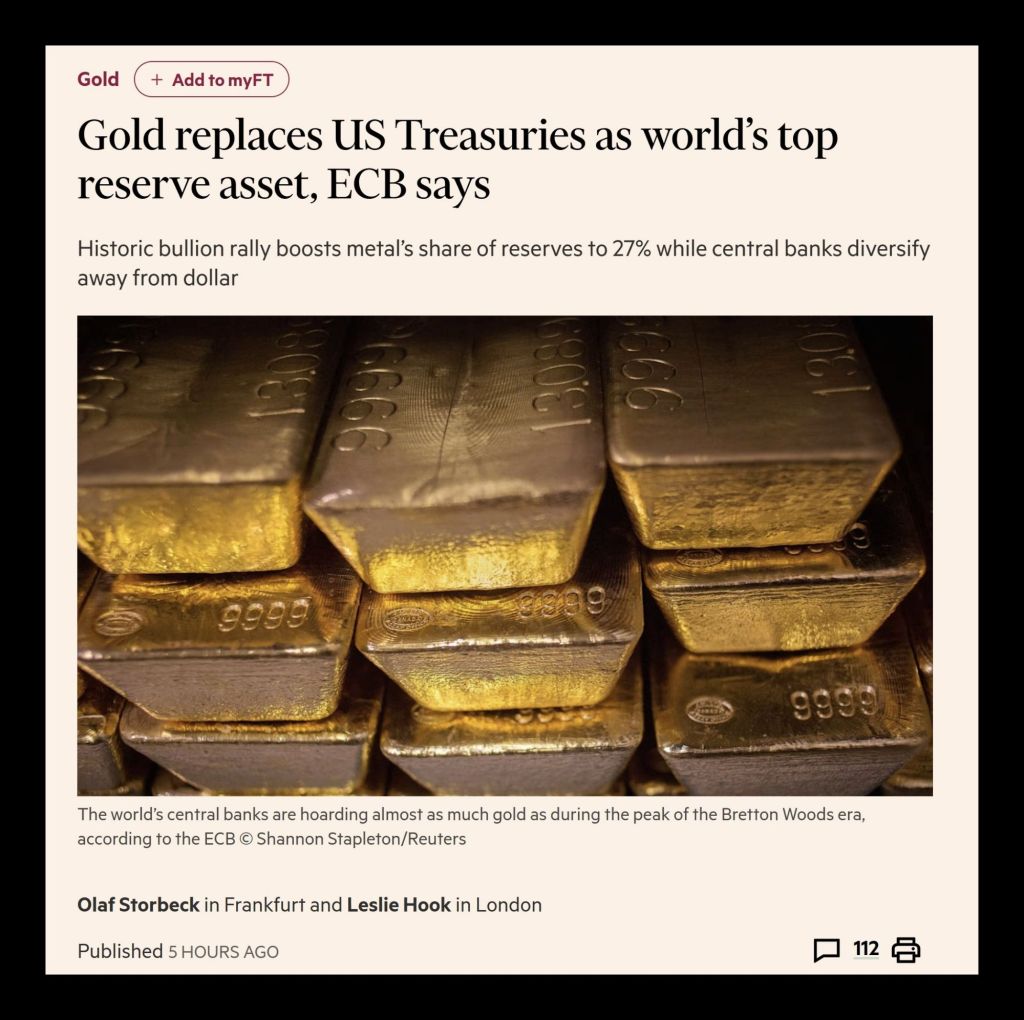

The second element of China’s financial counter-pressure concerns gold. The Hong Kong government established the Hong Kong Precious Metals Central Clearing Company, a wholly state-owned entity, and announced it would begin trial operations before the end of 2026, with a full system launch targeting July 2026. The Hong Kong Special Administrative Region government simultaneously signed a cooperation agreement with the Shanghai Gold Exchange and announced plans to expand Hong Kong’s gold storage capacity to more than 2,000 metric tonnes within three years. The objective, stated explicitly in Hong Kong Financial Secretary Paul Chan Mo-po’s public communications, is to create a credible alternative to the London Bullion Market Association and COMEX as the institutional benchmark for gold price discovery and settlement, concentrating Asia’s gold trading and clearing infrastructure in a jurisdiction outside Western legal reach. The Bullionstar analysis published in May 2026 identified the specific mechanism: China, already the world’s largest producer and consumer of gold, combined with Saudi Arabia’s growing practice of settling yuan-denominated oil transactions indirectly through gold, provides the infrastructure for oil sales to be settled in a currency and through a clearing system over which the United States Treasury and the Office of Foreign Assets Control have no jurisdiction. The petrodollar system’s foundational requirement, that oil be priced and settled in dollars, generating structural global demand for American currency and by extension American government debt, is being circumvented not through a direct confrontation but through the gradual construction of a parallel settlement architecture whose institutional components are being assembled in plain sight across multiple simultaneous moves.

The third element is the Euroclear development. On 2 February 2026, Euroclear announced it was supporting Crédit Agricole Corporate and Investment Bank and the Bank of China in the use of offshore Chinese government bonds as eligible collateral under triparty arrangements for uncleared margin requirements. Euroclear’s Asia Pacific CEO Philippe Laurensy stated that “onshore RMB bonds now represent a pool of high-quality collateral totalling approximately €5 trillion,” and that the institution was committed to “facilitating efficient, secure cross-border collateral flows” involving Chinese assets. Clearstream simultaneously enabled offshore Chinese government bonds as initial margin collateral for major international financial institutions. The Financial Times subsequently reported that Euroclear was planning to accept China onshore bonds traded in Hong Kong as eligible collateral in a further expansion of the arrangement. Euroclear is the backbone of international securities settlement, holding approximately €37 trillion in assets under custody and processing an estimated €1 quadrillion in transactions annually. When Chinese government bonds become accepted as standard high-quality collateral within Euroclear’s settlement infrastructure, they acquire a functional equivalence to cash within the plumbing of international finance. Sean Foo’s financial analysis, quoted by Crooke, identified the systemic implication with precision: “When Euroclear accepts Chinese bonds as collateral, those bonds are treated as equivalent to liquid cash. They are good enough to back all international transactions, meaning that the global financial plumbing will be incorporating Chinese debt into the core infrastructure.” China’s $26 trillion bond market, the second largest in the world, backed by $50 trillion in domestic bank deposits providing the deep domestic buyer base that bond markets require for stability, is being integrated into the foundations of the same settlement architecture that currently depends exclusively on American Treasuries as its risk-free benchmark collateral.

The combined effect of these three movements, withdrawing Chinese retail capital from American equity markets, constructing a Hong Kong gold clearing infrastructure capable of settling yuan oil transactions outside Western jurisdiction, and integrating Chinese government bonds into the core collateral infrastructure of international settlement, represents a financial architecture whose strategic coherence matches the geographic coherence of the overland BRI energy route attacks described elsewhere in this series. Washington’s response to the perceived Chinese economic challenge has been to raise Chinese capital and energy costs simultaneously: tariffs to raise capital costs, Hormuz blockade to raise energy costs, semiconductor export controls to constrain technology access. Beijing’s counter-response targets the financial infrastructure through which American dominance is sustained: the equity market flows that support American asset valuations, the gold pricing infrastructure that underpins the dollar’s reserve currency function, and the settlement architecture that makes American Treasuries uniquely attractive as global collateral. Crooke’s assessment that the Tehran war has marked a significant reshuffling of global geopolitics rests on the observation that these financial responses were not possible at scale before the Iran war created the political conditions, specifically, the demonstrated American willingness to disrupt global energy supply for strategic purposes, that removed whatever remaining inhibition Beijing may have felt about openly pursuing monetary system diversification. The war did not cause China’s financial counter-strategy. It removed the last argument against accelerating it.

Whether this restructuring produces a genuine transition in the international monetary system or remains a set of parallel and incomplete institutional developments depends on variables, including American political responses to financial market stress, the pace of yuan internationalisation, the durability of Saudi-Chinese energy arrangements, and the institutional depth of the Hong Kong gold clearing system, that cannot be resolved by analysis of the current situation alone. What can be stated with confidence is that the financial system through which American geopolitical leverage operates is, as of June 2026, simultaneously under pressure from three distinct and coordinated directions, that each pressure is being applied through legal and institutional mechanisms rather than through military or sanctions instruments, and that the GENIUS Act’s crypto-dollar strategy and the Hormuz blockade’s energy pressure campaign have produced a response whose financial sophistication suggests that China’s planning institutions had prepared these instruments in anticipation of precisely the kind of escalation that the Iran campaign represents.

The question of whether Washington’s strategic planners anticipated this specific response when they designed the campaign is one the available record does not yet answer.

Authored By: Global GeoPolitics

If you prefer to make a one time donation in support of my work, you can do so by clicking any link below:

https://buymeacoffee.com/ggtv |

https://ko-fi.com/globalgeopolitics |

Bitcoin: 3NiK8BoRZnkwJSHZSekuXKFizGPopkE7ns

References

Alastair Crooke, “Iran War Effect Marks the Resetting of World Geo-politics,” Strategic Culture Foundation / archive.ph, May 2026 – Velayati quote; zugzwang formulation; Beijing summit imagery; Genius/Clarity Act analysis; $50 trillion Chinese bank deposits; Euroclear Sean Foo quotes; Hong Kong gold trading centre

Ali Akbar Velayati, Senior Adviser to Iran’s Supreme Leader, public statement on Hormuz guarantee, cited in Crooke – “Geography does not lie” quote

Nahum Barnea, Yediot Ahoronot, cited in Crooke – “We are sliding into a never-ending war on three, perhaps four fronts”

US Congress, Guiding and Establishing National Innovation for US Stablecoins Act (GENIUS Act, S.394 / S.1582), signed into law 18 July 2025 Senate 68-30 vote 17 June 2025; House 308-122 vote 17 July 2025; stablecoin reserve requirements in US Treasuries

US Congress, Digital Asset Market Clarity Act of 2025 (Clarity Act, H.R. 3633), passed House with bipartisan support; Arnold & Porter advisory, July 2025

Brookings Institution, “Next Steps for GENIUS Payment Stablecoins,” March 2026 – reverse repurchase collateral mechanism; longer-dated Treasury demand; reciprocity provision analysis

State Street Global Advisors, “GENIUS Act Explained,” July 2025

CSRC, enforcement notice against Tiger Brokers, Futu Securities International, and Longbridge Securities, 22 May 2026 – China Money Network, 26 May 2026; Vision Times, 1 June 2026

Tiger Brokers and Futu combined fines 2.3 billion yuan / $330 million – Vision Times, 1 June 2026 · Eight-agency coordinated enforcement campaign – South China Morning Post, May 2026

$1 trillion hot money outflow 2025 – ZeroHedge, May 2026; $32 billion AUM mainland clients confirmed

HK$250 billion mainland investor assets in Hong Kong brokerages – SCMP / Citic Securities estimate

TheStreet, “US Investors Feeling Impact of Chinese Securities Crackdown,” 3 June 2026 – Wall Street foreign buyer dependency confirmed

CNBC, “China Is Making It Harder for Mom and Pop to Access US Stocks,” 3 June 2026 – shift to Hong Kong listings; CSRC Wu Qing regulatory campaign

California Wall Street, “China Tightens Access to US Stocks,” 3 June 2026

Hong Kong Government, establishment of Hong Kong Precious Metals Central Clearing Company (state-owned) – Nikkei Asia, cited in Kitco News, 4 March 2026

HKSAR Chief Executive John Lee, gold clearing announcement, cooperation agreement with Shanghai Gold Exchange, January 2026 – Global Times, January 2026

Hong Kong Financial Secretary Paul Chan Mo-po, post on OTC gold settlement efficiency, cited in Global Times

HKEX Gregory Yu, Legislative Council remarks on physical gold infrastructure, 5 May 2026 – Reuters, cited in Discovery Alert

Full launch targeting July 2026 – Discovery Alert, Hong Kong Gold Clearing House analysis, May 2026 · Gold storage expansion to 2,000 metric tonnes within three years – Kitco News / Nikkei Asia

Bullionstar / Ronan Manly, “China’s Golden Gateway: How the SGE’s Hong Kong Vault Will Shake Up Global Gold Markets,” 2026 – yuan oil settlement via gold; Saudi Arabia indirect gold-yuan mechanism

Euroclear press release, “Euroclear Supports Crédit Agricole CIB and Bank of China,” 2 February 2026 – offshore Chinese government bonds as collateral; €5 trillion onshore RMB bond pool; Philippe Laurensy CEO quote

Securities Finance Times, “Clearstream and Euroclear Broaden Access to Offshore Chinese Government Bonds as Collateral,” 2 February 2026

Financial Times, Euroclear plans to accept China onshore bonds traded in Hong Kong as collateral – cited in multiple May 2026 sources

China bond market $26 trillion / second largest globally – Securities Finance Times February 2026

Sean Foo financial analysis on Euroclear implications, cited in Crooke “global financial plumbing incorporating Chinese debt into core infrastructure”

BNY Mellon, Chinese bonds as tri-party repo collateral, Bloomberg, April 2021 – historical precedent for current expansion

World Economic Forum, “How Will the GENIUS Act Work in the US and Impact the World?”, July 2025 – Christine Lagarde ECB warning on dollar stablecoin threat to European monetary autonomy

Alastair Crooke background: former British diplomat, EU Special Envoy for the Middle East, senior MI6 officer, founder of Conflicts Forum

Leave a comment