How Governments and Markets Are Consuming Strategic Reserves to Bridge a Hormuz Disruption Whose End They Cannot Demonstrate

On 11 March 2026, the International Energy Agency coordinated the largest emergency strategic reserve release in history, drawing 400 million barrels from the stockpiles of 32 member nations, the United States contributing 172 million barrels from the Strategic Petroleum Reserve, as authorised by President Trump and announced by Energy Secretary Chris Wright. The release was described publicly as a stabilising measure to bring down oil prices following Iran’s closure of the Strait of Hormuz after the American and Israeli airstrikes on 28 February 2026. Macquarie analysts assessed the 400 million barrels in the context of what it was actually bridging: roughly four days of global oil consumption, or sixteen days of the volume that ordinarily transits the Gulf. “If that doesn’t sound like much,” the analysts stated, “it isn’t.” Within hours of the IEA announcement, Brent crude was trading back above $90 per barrel, as markets absorbed the arithmetic and concluded that the reserve release addressed approximately sixteen days of the disruption whose duration neither government nor market had honestly confronted.

The analytical framework through which governments, oil companies, and financial markets have been operating since the disruption began was characterised with unusual precision by Jim Bianco of Bianco Research. Every major crisis in the modern era, the Asian financial contagion of 1997, the credit collapse of 2008, the pandemic shock of 2020, began with the same institutional misdiagnosis, treating a structural problem as a temporary liquidity glitch. Wall Street’s institutional culture is, by Bianco’s account, hardwired to assume mean reversion. The profession has been conditioned to fear the phrase “this time is different” through years of false alarms, failed predictions, and the profitable habit of buying dips that the central bank backstop reliably validated. The consequence is an institutional bias against recognising the class of problem that genuinely does not revert to the mean and Bianco’s assessment of the Hormuz situation is that governments and oil companies are now aggressively draining inventories on the premise of a 60-day disruption, treating a potential permanent structural deficit in the world’s crude supply as a short-term liquidity problem whose resolution can be assumed rather than demonstrated. Burning the lifeboats, as he describes it, only works if a resolution is guaranteed. By artificially delaying gradual demand destruction today, the process ensures it arrives all at once should inventories reach operational minimums without the strait having reopened.

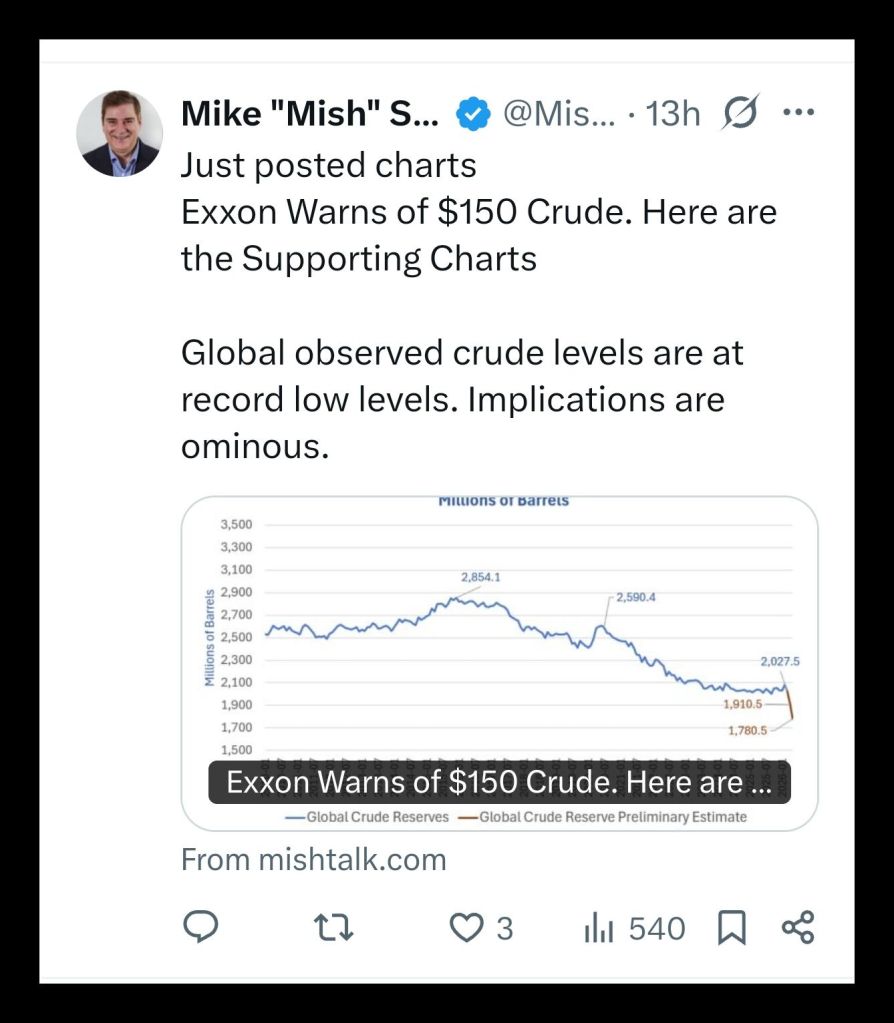

The physical arithmetic of the disruption places the severity of the misdiagnosis in measurable terms. Approximately 20.5 million barrels per day transited the Strait of Hormuz under normal conditions, representing roughly twenty percent of global crude oil supply and forty percent of internationally traded crude, according to United States Energy Information Administration data. The effective loss after accounting for existing bypass infrastructure, the Petroline and East-West pipelines across Saudi Arabia, the Abu Dhabi Crude Oil Pipeline, and available tanker rerouting capacity, amounts to a structural shortage of between seven and twelve million barrels per day according to LNRG Technology’s analysis of pipeline bypass capacities, after bypass pipelines absorb approximately four to seven million barrels per day. Global oil inventories were, according to the International Energy Agency, being drawn down at an average rate of 8.5 million barrels per day during the second quarter of 2026. In March 2026 alone, drawdown accelerated from 5.27 to 8.62 million barrels per day. Veteran energy analyst Paul Horsnell estimated that cumulative global inventory losses could approach 1.2 billion barrels if current drawdown trajectories were maintained, with commercial storage systems potentially reaching minimum operating levels as early as August 2026. The Strategic Petroleum Reserve itself was at 58 percent of capacity before the crisis began, following the Biden administration’s 2022 drawdown, with ongoing facility repairs constraining refill rates. The 172 million barrels committed by the United States are structured as an exchange rather than a permanent release, borrowed barrels that must be returned between November 2026 and September 2028, at premium return rates of 18 to 22 percent. The lifeboats being burned have a repayment schedule attached.

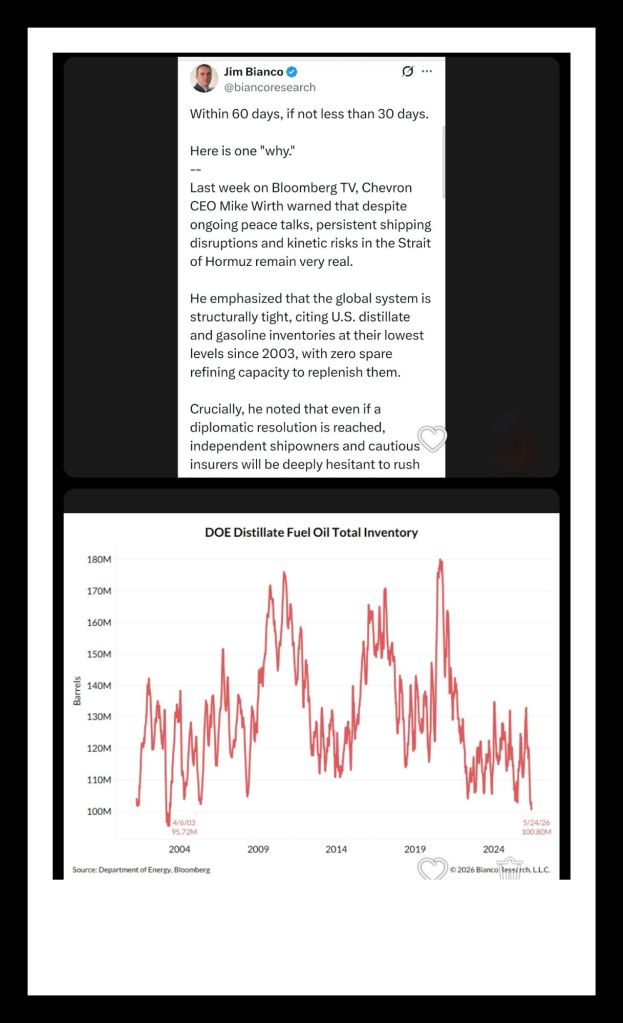

Art Berman, a petroleum geologist with forty years of industry experience and a degree in Middle Eastern history, described the Hormuz disruption in his 27 March 2026 blog post as a physical system failure rather than a price story. “This is not a price story, it is a physical system failure,” Berman wrote. “The world’s most important energy chokepoint is impaired at a scale without precedent. Energy is the economy, and when the primary artery is disrupted, the system begins to break down.” Berman’s analysis differentiated carefully between a market that is managing a crisis and one that is disguising it through inventory consumption, noting that when the disguise runs out, the transition tends to be abrupt rather than gradual. Subsequent interviews on The Great Simplification in May 2026 developed this analysis further: even in the scenario most favourable to rapid resolution, the strait reopening immediately, logistical constraints including de-mining operations, insurance market recovery, tanker queue clearance, and refinery supply chain normalisation meant that oil would not flow at pre-war volumes until late 2026 at the earliest. The lag between physical resolution and market normalisation was, in Berman’s assessment, itself a structural feature of the crisis that financial markets had substantially failed to price. The market, as Art Berman observed to Bianco’s framework: “No credible analysis suggests Hormuz will reopen soon or that tanker flows will return to pre-war levels. That’s the reality markets should be pricing and policymakers should be planning for.”

The Federal Reserve’s position illustrates the institutional bind that the structural-versus-liquidity misdiagnosis creates for monetary policy. Jim Bianco’s April 2026 analysis for Financial Sense identified the core contradiction: the Fed faced a choice between fighting oil-driven inflation through higher interest rates, which would deepen the economic contraction that the energy shock was already producing, or accepting structurally elevated inflation to avoid compounding the supply-side damage through demand suppression. The futures market by late May 2026 was pricing Fed hikes while the Fed’s own guidance continued to signal cuts, a divergence Bianco described as the market having concluded that Kevin Warsh, confirmed as Federal Reserve Chair, had not yet aligned the institution’s forward guidance with the inflationary trajectory the oil market was actually embedding. The United States national average gasoline price had risen from $2.98 per gallon before the war to $4.45 by late April, a roughly 49 percent increase, adding approximately $25 per fill-up for the average American driver. American consumers were absorbing the price shock, but the shock was not translating into visible fuel shortages in the United States because the demand destruction was occurring predominantly elsewhere, in the Asian import-dependent economies including the Philippines, Thailand, Malaysia, Indonesia, and South Korea, which depended on Middle Eastern imports for between sixty and ninety-five percent of their oil needs and faced the price rationing that Bianco described with blunt accuracy, that somebody has to not consume ten to fifteen million barrels of oil per day, and it happens through price rather than policy.

The market’s inability to price the structural character of the disruption reflects a specific historical conditioning that Bianco’s crisis comparison identifies. Over the five years preceding the Iran war, professional macro investors accumulated what he described as deep scar tissue from listening to experts warn of systemic disruption. The pandemic oil price collapse of 2020 recovered within a year. The Russian invasion of Ukraine in 2022 produced an energy shock that European governments managed through accelerated LNG diversification and demand reduction without triggering the economic catastrophe that early analysis had projected. The Houthi Red Sea attacks in 2023 and 2024 caused shipping disruptions that rerouted vessels around the Cape of Good Hope, adding cost and time but not producing the supply crisis that commentators anticipated. Each episode trained the institutional reflex toward scepticism of the worst-case analysis and toward buying the dip. The problem with the current situation, as Bianco’s framework explicitly identifies, is that the absence of a credible diplomatic pathway to strait normalisation, a feature of the current crisis that distinguishes it from its predecessors, converts what the market is treating as a 60-day disruption into something potentially far longer. There is no prior Iran war of this scale in the modern era; the 1973 Arab oil embargo lasted approximately five months and involved a cartel decision rather than a military occupation of a waterway; the 1979 Iranian Revolution reduced Iranian exports rather than closing a transit chokepoint; and none of the historical precedents involved the simultaneous presence of an active American naval blockade on the same waterway where the disruption was occurring.

The Dallas Federal Reserve’s March 2026 economic analysis modelled the disruption under varying duration assumptions, noting that if the closure persisted for three quarters, roughly the duration of the 1973 oil supply disruption, the probability of the strait remaining closed in the third quarter of 2026 was 58 percent and in the fourth quarter 35 percent. The model explicitly declined to project actual closure duration, acknowledging that no credible basis for projection existed. That intellectual honesty from the Federal Reserve Bank of Dallas contrasts starkly with the operational behaviour of the oil market, which was pricing December 2026 Brent futures at above $90 per barrel and June 2027 futures at above $80, a futures curve that Bianco described as representing the market’s grudging concession that the disruption would persist for longer than the 60-day assumption embedded in the physical inventory strategy, but still falling well short of pricing any scenario approaching a multi-quarter structural closure. UBS analysts warned by late May 2026 that oil inventory buffers had been “largely exhausted” and highlighted the “risk of panic buying if physical dislocation intensifies and the Strait of Hormuz remains closed,” a formulation that identified the precise mechanism Bianco had described: gradual demand destruction delayed by inventory drawdown transforms, at the point of inventory exhaustion, into abrupt and severe price dislocation.

The question of whether the governments and institutions managing the crisis possess the analytical framework required to act on the structural diagnosis is separate from the question of whether the diagnosis is correct. The IEA’s own coordinated release, four days of global consumption deployed against a disruption entering its fourth month, suggests that the structural character of the problem had not penetrated the operational planning of the primary institutional responders. Energy Secretary Chris Wright’s framing of the SPR release as a price-lowering measure structurally identical to the Biden administration’s 2022 post-Ukraine drawdown suggests that the Trump administration was treating an energy supply crisis of systemic character through the political management tools developed for inflationary episodes of far smaller magnitude. The exchange structure requiring premium repayment of 18 to 22 percent between November 2026 and September 2028 means the United States government committed to replenishing its primary emergency energy reserve during the period when, on the Dallas Fed’s own probability calculations, the disruption would still have a non-trivial probability of continuation. Berman’s description of the crisis as a forcing mechanism that could compress decades of needed structural adjustment into months was not framed as a forecast to be welcomed. The adjustment he describes, demand destruction of a scale sufficient to rebalance supply and consumption without strait normalisation, occurs not through policy but through the mechanism of prices rising until marginal consumers are forced out of markets they can no longer afford to participate in. That process was, as of the final days of May 2026, measurably underway and measurably underpriced.

Authored By: Global GeoPolitics

If you prefer to make a one time donation in support of my work, you can do so by clicking any link below:

https://buymeacoffee.com/ggtv |

https://ko-fi.com/globalgeopolitics |

Bitcoin: 3NiK8BoRZnkwJSHZSekuXKFizGPopkE7ns

References

Jim Bianco, LinkedIn post on structural vs liquidity misdiagnosis (May 2026) – “burning the lifeboats” formulation; 60-day hurdle framing; scar tissue analysis; crisis comparison 1997/2008/2020

Jim Bianco, Financial Sense Newshour, “Oil Spikes Past $90: Inflation Risks, Credit Spreads, and AI Upheaval,” 6 March 2026 – backwardation analysis; $90 front month vs $72 August; short-term disruption pricing

Jim Bianco, Financial Sense Newshour, “High-Stakes Stand-Off: Iran’s Pain Threshold and Divided Fed,” 30 April 2026 – demand destruction mechanism; “somebody has to not fill up their car”; Fed hike vs cut divergence; IRGC incentive analysis

Jim Bianco, Financial Sense Newshour, “Jim Bianco’s Biggest Miscalculation on Iran,” May 2026 – “we in the West underestimate the amount of pain the Iranian regime is willing to endure”; January protest crackdown

Jim Bianco / Bianco Research, X (@biancoresearch) – 10-year yield 4.60% highest since Trump took office; Warsh Fed alignment; Dec 2026 and Jun 2027 Brent futures at new highs

Art Berman, “A System Failure is Not an Oil Bull Market,” artberman.com, 27 March 2026 – “physical system failure not a price story”; 2011–2014 analogue rejected; debt-saturated economy context

Art Berman, The Great Simplification Episode 220: “A World on the Precipice: The Last Oil Tanker from the Strait of Hormuz has Arrived – Now What?”, 13 May 2026 – even if war ends today, logistics mean no supply normalisation until late 2026; de-mining, insurance, tanker queue lags

Art Berman, Palisades Gold Radio, “Coming Oil Shock ‘Worst Thing’ in Modern History, Shortages Inevitable,” 24 May 2026 – 15–20 mb/d gross flow; 10 mb/d effective loss after bypass; “world economy losing 20% of its blood daily”

US Department of Energy, Energy Secretary Chris Wright statement on SPR release, 11 March 2026 – 172 million barrels; 120 days delivery; exchange structure confirmed; “at no cost to the taxpayer”

US Department of Energy, Emergency Exchange RFP, 13 March 2026 – 86 million barrels first tranche; 18–22% premium return; November 2026 to September 2028 return window

IEA coordinated release announcement, 11 March 2026 – 400 million barrels from 32 nations; largest ever IEA release; Germany, Austria, Japan contributions

US Energy Information Administration, “DOE Has Released 17.5 Million Barrels from the Strategic Petroleum Reserve Since March,” 30 April 2026

Al Jazeera, “IEA Agrees to Release 400 Million Barrels of Oil from Strategic Reserves,” 11 March 2026 – Macquarie “four days of global production” and “16 days of Gulf volume” assessment; Brent back above $90 after announcement

Institute for Energy Research, “US Will Release 172 Million Barrels of Oil From the Strategic Petroleum Reserve,” 13 March 2026 – SPR at 58% capacity pre-crisis; Biden facility damage; refill constraints

Mineral Rights Podcast, “Running on Empty: The US Strategic Petroleum Reserve,” 26 March 2026 – WTI $67 on 27 February to $98.71 on 13 March (47% in two weeks); exchange vs permanent sale confusion

LNRG Technology, “2026 Hormuz Strait Disruption: Oil Market Impacts and Supply Risks,” 15 March 2026 – bypass capacity 4–7 mb/d; structural shortage 7–12 mb/d; 630–1,080 million barrel cumulative 3-month shortfall

IEA Gas Market Report Q2 2026 – global oil inventory drawdown 8.5 mb/d average Q2 2026; steepest draws May–June; Brent ~$106

OilPrice.com, “IEA Revises 2026 Forecast: Oil Deficit Widens as Iran War Cuts Production,” May 2026 – March drawdown 5.27 to 8.62 mb/d; Iraq, Saudi Arabia, Kuwait, UAE output cuts

Paul Horsnell cited in Discovery Alert, “Oil Supply Crunch: Inside the Strait of Hormuz Crisis 2026,” 30 May 2026 – 1.2 billion barrel cumulative loss projection; minimum operating levels August 2026

UBS inventory warning, cited in CleanTechnica, 31 May 2026 – “buffers largely exhausted”; “panic buying risk if physical dislocation intensifies”

Dallas Federal Reserve, “What the Closure of the Strait of Hormuz Means for the Global Economy,” 20 March 2026 – probability models; 3-quarter 1973 analogue; 58% Q3 / 35% Q4 closure probability

Discovery Alert, “How the Strait of Hormuz Closure Is Driving Oil Prices in 2026,” May 2026 – $154/bbl at 12 weeks; 5.3 mb/d shortfall estimate; CSIS geography analysis

BrentChart.com, “Understanding the 10 Million Barrel Daily Oil Shortfall: Strait of Hormuz Closure Analysis,” March 2026 – 120 days SPR minimum operational level; 10 mb/d net shortfall confirmed

NBC News, “Major Multi-Country Oil Release Deal Fails to Bring Down Petroleum Prices,” 12 March 2026

US national average gasoline price data: $2.98 pre-war to $4.45 (Financial Sense / Bianco Research, April 2026)

Leave a comment